Self-made millionaire David Bach was quoted in a CNBC article explaining that “the single biggest mistake millennials are making” is not purchasing a home because buying real estate is “an escalator to wealth.”

Bach went on to explain:

“If millennials don’t buy a home, their chances of actually having any wealth in this country are little to none. The average homeowner to this day is 38 times wealthier than a renter.”

In his bestselling book, “The Automatic Millionaire,” Bach does the math:

“As a renter, you can easily spend half a million dollars or more on rent over the years ($1,500 a month for 30 years comes to $540,000), and in the end wind up just where you started — owning nothing. Or you can buy a house and spend the same amount paying down a mortgage, and in the end wind up owning your own home free and clear!”

Who is David Bach?

Bach is a self-made millionaire who has written nine consecutive New York Times bestsellers. His book, “The Automatic Millionaire,” spent 31 weeks on the New York Times bestseller list. He is one of the only business authors in history to have four books simultaneously on the New York Times, Wall Street Journal, BusinessWeek and USA Today bestseller lists.

He has been a contributor to NBC’s Today Show appearing more than 100 times, has been a regular on ABC, CBS, Fox, CNBC, CNN, Yahoo, The View, and PBS, and has been profiled in many major publications, including The New York Times, BusinessWeek, USA Today, People, Reader’s Digest, Time, Financial Times, The Washington Post, The Wall Street Journal, Working Woman, Glamour, Family Circle, Redbook, Huffington Post, Business Insider, Investors’ Business Daily, and Forbes.

Bottom Line

Whenever a well-respected millionaire gives investment advice, people usually clamor to hear it. This millionaire gave simple advice – if you don’t yet live in your own home, go buy one. I can’t say it better than that! Questions? Feel free to ask. As always, I’m here to help!

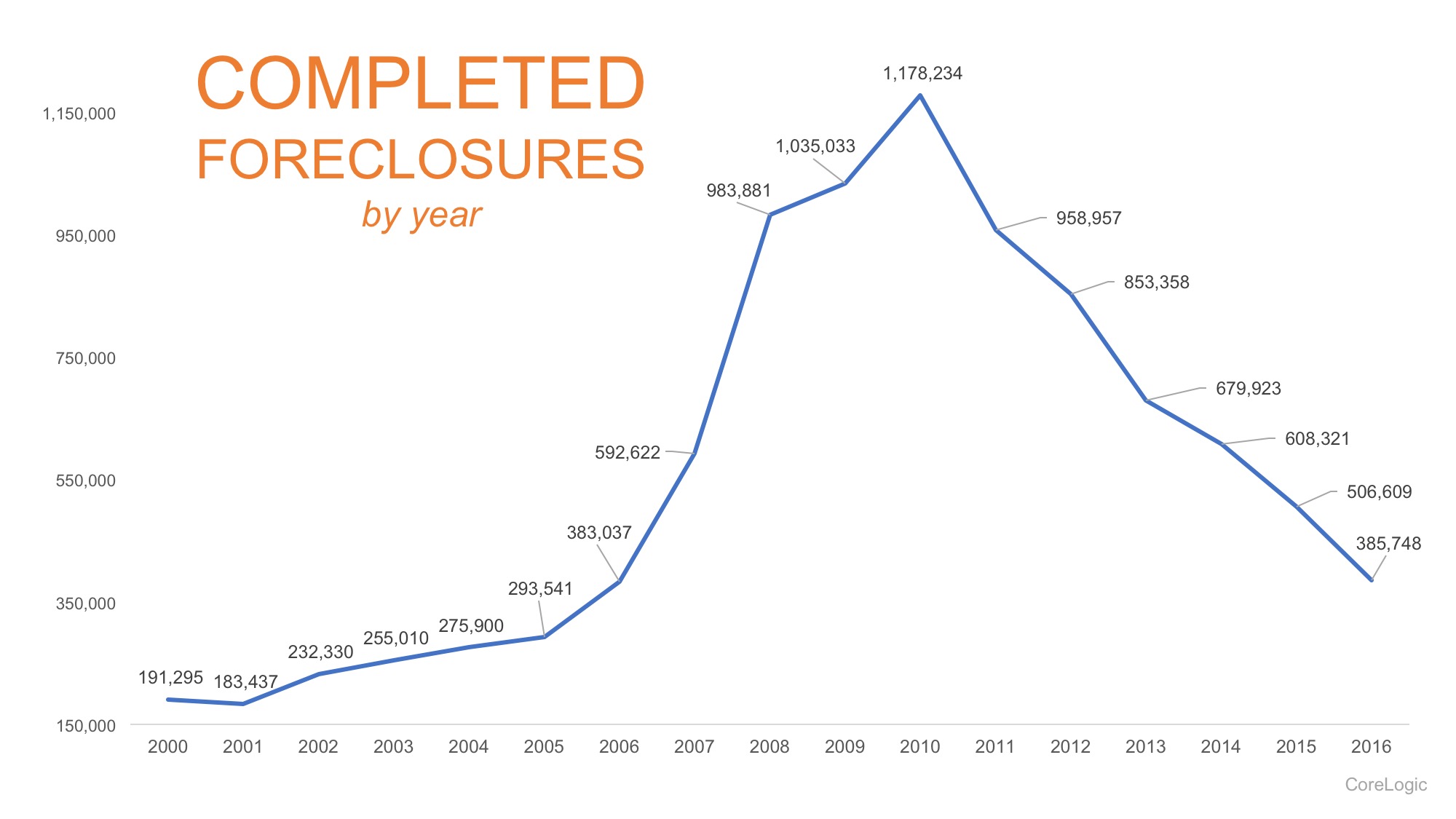

CoreLogic recently released a report entitled, United States Residential Foreclosure Crisis: 10 Years Later, in which they examined the years leading up to the crisis all the way through to the present day. With a peak in 2010 when nearly 1.2 million homes were foreclosed on, over 7.7 million families have lost their homes throughout the entire foreclosure crisis.

Dr. Frank Nothaft, Chief Economist for CoreLogic, had this to say,

“The country experienced a wild ride in the mortgage market between 2008 and 2012, with the foreclosure peak occurring in 2010. As we look back over 10 years of the foreclosure crisis, we cannot ignore the connection between jobs and homeownership. A healthy economy is driven by jobs coupled with consumer confidence that usually leads to homeownership.”

Since the peak, foreclosures have been steadily on the decline by nearly 100,000 per year all the way through the end of 2016, as seen in the chart below. This is good news for many who have struggled through these years. The crisis is not over, but it has declined to the point where distressed properties now comprise a very small percentage of the entire housing market.

If this trend continues, the country will be back to 2005 levels by the end of 2017. Whether or not we will achieve the low levels experienced in 2001, and how long that might take, remains to be seen.

Bottom Line

As the economy continues to improve and employment numbers increase, the number of completed foreclosures should continue to decrease. A strong housing market has been and will continue to be intricately intertwined with a strong economy. Questions? Please ask. As always, I am here and happy to help!

In many areas of the country, there are not enough homes for sale to satisfy the number of buyers looking to purchase their dream homes. Here in the Puget Sound area, buyer demand continues to push prices to new highs as purchasers compete for low inventory. Experts have long proposed that a ramp-up in new, single-family home construction would be one of the many ways to overcome this inventory shortage and lead to a more balanced market.

According to a recent survey conducted by the National Association of Home Builders (NAHB) and Wells Fargo, housing market confidence among builders reached an 11-year high last month.

What Does High Confidence Mean for the Housing Market?

In a recent interview, Rob Dietz, Chief Economist and SVP for NAHB, put it this way:

“Higher market confidence will translate into more building and more inventory in 2017. We expect single-family construction to grow 10 percent next year.”

With 2016 marking the best year in real estate sales in over a decade, a 10 percent ramp-up in single-family construction will aid in making 2017 an even greater year. In most areas of Kitsap County, new construction is booming and home sales across all price ranges remain strong.

According to the latest US Census data, sales of newly constructed homes were up 3.7% over January 2016 nationwide as they reached a seasonally adjusted annual rate of 555,000. Dietz went on to comment:

“We can expect further growth in new home sales throughout the year, spurred on by employment gains and a rise in household formations. As the supply of existing homes remains tight, more consumers will turn to new construction.”

Bottom Line

With the weather and the real estate market heating up this spring, there will be a surge of new construction coming to the market soon. New development may already be underway in your neighborhood. Interested in knowing more or have questions? As always, feel free to ask. I’m here to help!

There is no doubt that historically low mortgage interest rates were a major impetus to the housing recovery we’ve seen over the last couple of years. However, many industry experts are showing concern about the possible effect that rising rates will have moving forward.

The Mortgage Bankers Association, Fannie Mae, Freddie Mac and the National Association of Realtors are all projecting that mortgage interest rates will move upward in 2017, and we’ve already seen a trend in that direction. Increasing interest rates will definitely impact purchasing power and may stifle demand. The questions are, when and by how much?

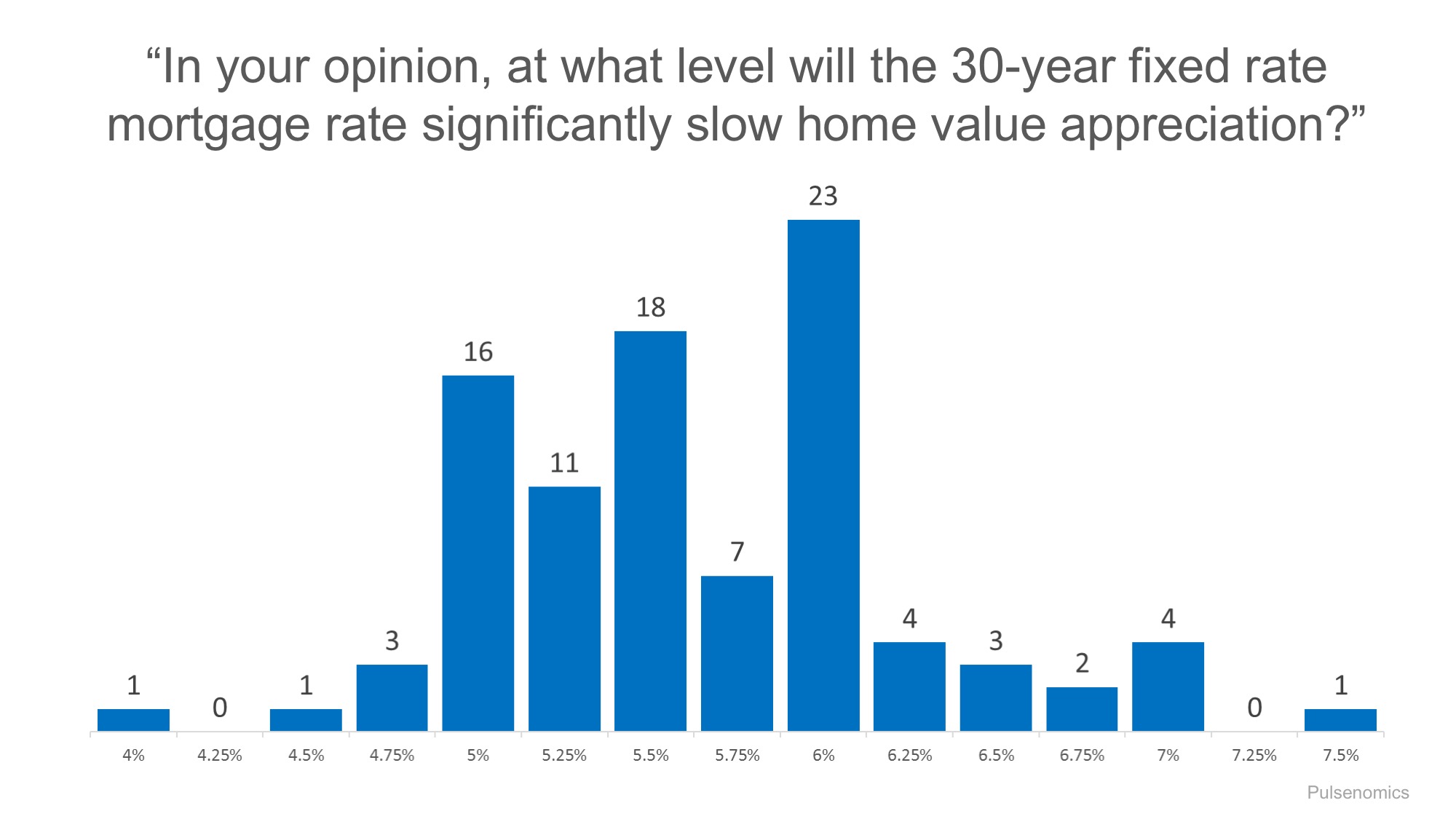

In a recent study of industry experts, “rising mortgage interest rates, and their impact on mortgage affordability” was named by 56% as the force they think will have the most significant impact on U.S. housing in 2017. If rising rates slow demand for housing, home values will be impacted. Areas such as ours, with a Seller’s market, may move to a more balanced market. Areas already in balance may see values slow or even stop, making home ownership options more attractive to buyers.

To this point, Pulsenomics, recently surveyed a panel of over 100 economists, investment strategists, and housing market analysts, asking the question “In your opinion, at what level will the 30-year fixed rate mortgage rate significantly slow home value appreciation?” The survey revealed the following:

Bottom Line

Of the panel members, most believe that rates would need to hit 5% or above to have an impact on home prices. Benchmarks at 5%, 5.5% and 6% had the majority of experts seeing changes in home values with 6% having the most votes. Rising rates will affect purchasing power, and home values may need to moderate to accommodate more limited demand. However, rates are and may remain at historically low levels for some time to come, and so far demand in our area has not slowed. Job availability and the underlying economy will definitely play a role in how quickly buyers adjust to new rates and payment options, and that will also play a role in supply and demand. Do you have questions? Please feel free to ask. As always, I’m here and happy to help!

Until today, I had not given much thought to the idea that owning a home has an impact on physical health. However, once I read the information contained in a recent NAR study, I realized the benefits are not limited to the financial aspects of owning your own home. Some of the results seem obvious, but some of the differences were surprising to me, including the significant differences in overall health outcomes.

“Owning a home embodies the promise of individual autonomy and is the aspiration of most American households. Homeownership allows households to accumulate wealth and social status, and is the basis for a number of positive social, economic, family and civic outcomes.”

Below I have included the section of the report that quoted several studies concentrating on the impact homeownership has on the health of family members. Here are some of the major findings on this issue revealed in the report:

There is a strong positive relationship between living in poor housing and a range of health problems, including respiratory conditions such as asthma, exposure to toxic substances, injuries and mental health. Homes of owners are generally in better condition than those of renters.

Findings reveal that increases in housing wealth were associated with better health outcomes for homeowners.

Low-income people who recently became homeowners reported higher life satisfaction, higher self-esteem, and higher perceived control over their lives.

Homeowners report higher self-esteem and happiness than renters. For example, homeowners are more likely to believe that they can do things as well as anyone else, and they report higher self-ratings on their physical health even after controlling for age and socioeconomic factors.

Renters who become homeowners not only experience a significant increase in housing satisfaction but also obtain a higher satisfaction even in the same home in which they resided as renters.

Social mobility variables, such as the family financial situation and housing tenure during childhood and adulthood, impacted one’s self-rated health.

Homeowners have a significant health advantage over renters, on average. Homeowners are 2.5 percent more likely to have good health. When adjusting for an array of demographic, socioeconomic, and housing–related characteristics, the homeowner advantage is even larger at 3.1 percent.

Bottom Line

People often talk about the financial benefits of homeownership. I have shared information on that topic more than once because it is so significant. As you can see, there are also meaningful social and health benefits to owning your own home. Is homeownership part of your dream? If so, take the first step and contact a great real estate professional for assistance in getting started. And, as always, if I can answer any questions for you or help in any way, feel free to ask. I’m here to help!

The media is full of messages right now encouraging home buyers to shop online for a home loan, to make lenders compete for your money, and to take advantage of quick-and-easy, impersonal mortgage application processes. But is that really a strategy for success, or is it a recipe for disaster? How important IS your mortgage loan when shopping for your dream home?

Real Estate is a Team Sport

Every home purchase is unique, and the process of buying or selling a home is complex. In an active, competitive housing market such as ours, the complexities increase. Two sides, buyers and sellers, have similar goals – the sale of an available home to a ready, willing, and able buyer. Transactions include homeowners, home purchasers, real estate professionals, mortgage lenders (the institution) as well as loan officers (the individuals), appraisers, inspectors, title companies, escrow companies, and more. In order to fulfill the desires of buyers and sellers, these groups and individuals have to work together to accomplish a common goal – the transfer of real property according to a contract and on time. Any failure in the chain of events necessary to make this happen can have major legal, financial and emotional consequences for all concerned.

People You Know, Like & Trust

While more and more people switch from brick-and-mortar stores to shopping online, one thing remains the same. People continue to prefer to do business with individuals they know, like, and trust. So – what does this have to do with obtaining a mortgage online?

Advertised percentage rates aren’t always the best deal. Independent mortgage companies and locally-owned banks often can meet or beat rates found online, and they may have loan products that better serve your needs. However, unless you connect with a local lender, you may not be able to take advantage of what they have to offer.

Online financial institutions may provide the funding for your loan, but your assigned loan officer is the individual responsible for ensuring your loan is processed and funded and your purchase is completed. In an anonymous online application system, you have no way of knowing how experienced or successful your loan officer is, nor will you know how likely they are to help you succeed.

Sellers rely on their listing agents to guide them through the process of accepting the best offer on their home. While there are many things to consider when reviewing any offer, the primary consideration is most often your pre-approval letter and the financing addendum – what type of financing is being provided, and who is providing it? When reviewing two offers alike in every way EXCEPT the lender, brokers will most often encourage sellers to choose the offer with financing provided by the loan officer and lending institution they know and trust to get the job done.

Bottom Line

While applying for a home loan in front of your laptop in your boxer briefs may sound appealing, it may not be the recipe for success you hoped it would be. Finding the home of your dreams only to lose it due to financing can be heartbreaking. Selecting a great real estate professional to guide you through the home buying or selling process is the best first step you can take. The next great step you can take is selecting a known and trusted local lender to help you finance your home. Asking your real estate professional for suggestions for lenders that are known, liked and trusted in your area is a smart, strategic move. And, as always, if you have questions please feel free to ask. I’m here to help!

The residential housing market all around Puget Sound has been hot, and Kitsap County is no exception. Home sales have bounced back solidly and are now at their second highest pace since February 2007. Demand has remained strong throughout the winter as many real estate professionals are reporting bidding wars with many homes selling above list price, and there doesn’t appear to be an end in sight any time soon. So – what about your house?

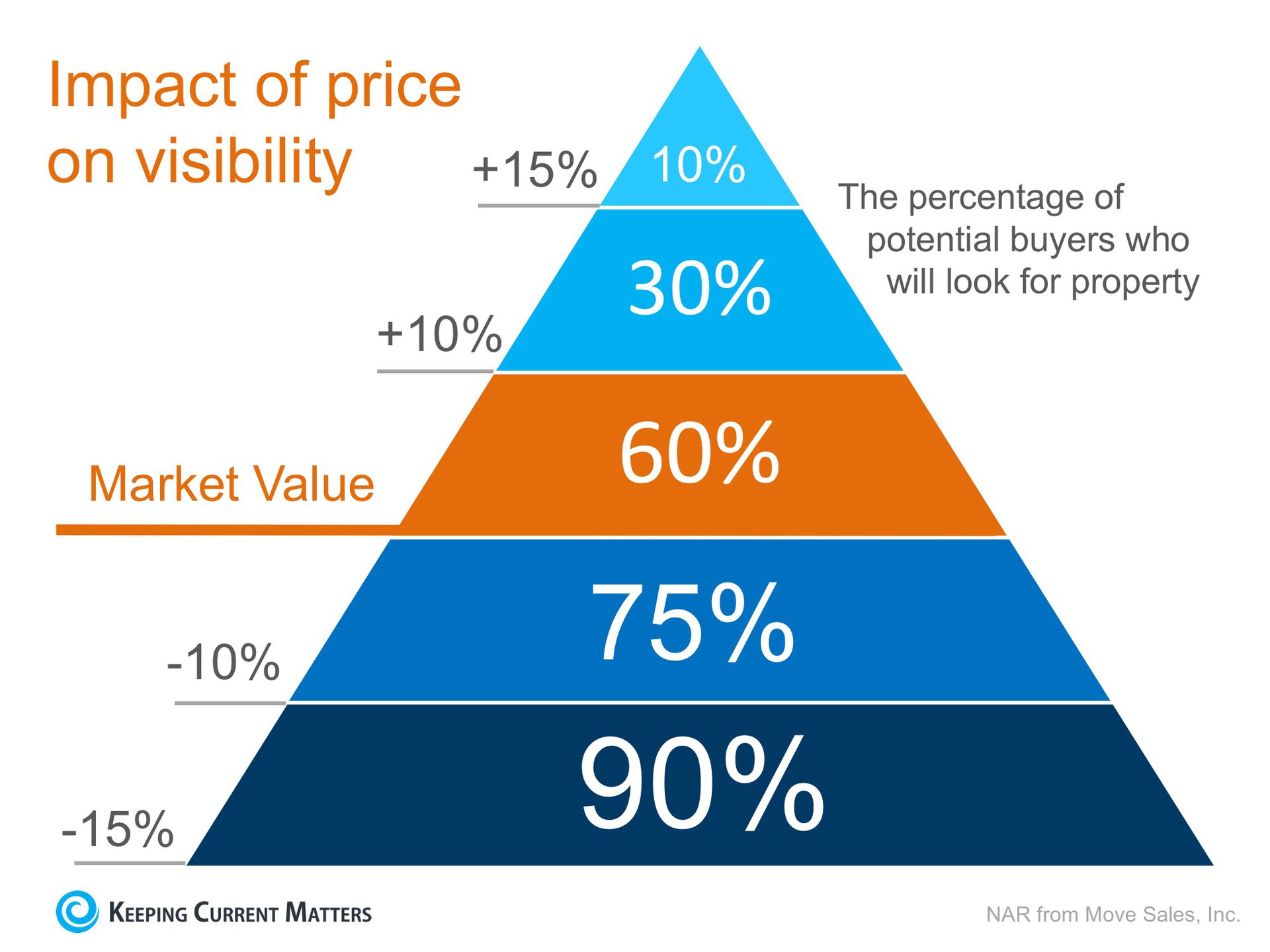

If your house hasn’t sold, it is most likely because of the price.

Home pricing is an art form as well as a science. Your real estate professional should be able to assist you in finding that “sweet spot” for selling your home at a price that attracts potential buyers while maximizing your return. If your home is on the market and showings are few or you are not receiving any offers, look at your price. Pricing your home just 10% above market value dramatically cuts the number of prospective buyers that will even see your house. Pricing it just 15% over market value will bring only a very small percentage of active buyers to your door. Other factors that may influence buyers (location, condition, presentation) should all be factored into and reflected in your sales price. See chart below.

C

Bottom Line

The housing market is hot. If your property is not, something is wrong. Buyers and the Brokers who represent them are price conscious as well as price savvy, and value is the #1 factor in attracting potential buyers. If you are not seeing the results you want, sit down with your real estate professional and revisit the pricing conversation. Adjustments in condition may need to be made to support the value, or your price may need to be adjusted to fit with the market. Overpriced houses that sit for long periods of time become stale, and when they do sell they are often undervalued because of time on the market. We don’t want this to happen to you! Do you have questions? Please feel free to ask. As always, I am here and happy to help!

Have you ever been flipping through the channels, only to find yourself glued to the couch in an HGTV binge session? We’ve all been there… watching entire seasons of “Love it or List it,” “Fixer Upper,” “House Hunters,” “Property Brothers,” and so many more, just in one sitting. These shows can be addictive!

When you’re in the middle of your real-estate-themed-show marathon, you might start to think that what you see on TV must be how it works in real life. If you are even tempted to believe what you see, you may need a reality check.

Reality TV Show Myths vs. Real Life:

Myth #1: Buyers look at 3 homes and make a decision to purchase one of them.

Truth: There may be buyers who fall in love with and buy the first home they see, or even one of the first three, but according to the National Association of Realtors the average home buyer tours 10 homes as a part of their search. Finding the right home, in the right location, for the right price doesn’t always – or even often – happen easily. Home buying is most often a time-consuming process.

Myth #2: The houses the buyers are touring are still for sale.

Truth: The reality is being staged for TV. Many of the homes being shown are already sold and are off the market. There simply aren’t a sufficient number of desirable homes active on the market to meet the needs of filming a reality TV show.

Myth #3: The buyers haven’t made a purchase decision yet.

Truth: Since there is no way to show the entire buying process in a 30-minute show, TV producers often choose buyers who are further along in the process and have already chosen a home to buy. The buyers are hand-picked to promote an image and processes are streamlined for viewer consumption.

Myth #4: If you list your home for sale, it will ALWAYS sell at the Open House.

Truth: Of course this would be great! Open houses are important to help provide the most exposure to buyers in your area, but open houses are only a PIECE of the overall marketing of your home. Just realize that most homes are sold during regular listing appointments by diligent Brokers working hard on behalf of their buyers.

Myth #5: Homeowners make a decision about selling their home after a 5-minute conversation.

Truth: Similar to the buyers portrayed on the shows, many of the sellers have already spent hours deliberating the decision to list their homes and move on with their lives/goals. In real life, sellers often spend time identifying the right Broker, right price, and right conditions necessary to list and sell their home in a way that best meets their needs.

Bottom Line

There is more to buying and selling a home than TV can portray, and we didn’t even touch on investment properties! Having an experienced professional on your side while navigating the real estate market is the best way to guarantee that you can make the home of your dreams a reality. And as always, if you have questions, please feel free to ask. I am here to help!

Kitsap County has been a “hot market.” Depending on the specific neighborhood, multiple offers, escalated prices, and cash deals have been common. Even in the hottest markets, though, selling a house is by no means a transaction that happens overnight. Every step—from listing your house to getting an offer to finally closing—takes time. But how much time?

To help you pace yourself, here are the major steps to selling a house, and how long each one typically takes so you can plan accordingly. Depending on where you live, you may need to settle in for a long ride…or a speedy turnaround!

How long does it take to list a home?

Answer: 3 to 5 days, perhaps longer

It will take your listing agent a few days or a bit longer to gather all the necessary info on your home (e.g., square footage, special features), help you plan cleaning and repairs, and arrange staging and photos. But once your agent has it all, things generally happen quickly. Once you have a signed listing agreement and all pieces are in place and ready to go, your agent will then upload these details onto the multiple listing service, which will make the listing viewable to agents. A shorter, consumer-friendly version of the MLS listing will also appear on sites like realtor.com®—and since this site refreshes its data at least every 15 minutes, your home will be in front of plenty of eyeballs in no time at all.

How long does it take to get an offer on a home?

Answer: on average from 0-65 days

The current average age of properties in general on the market is 65 days. That said, this varies greatly by location and time of year, so there’s no one right answer to how long you’ll wait for that blessed first offer. Kitsap County homes are moving quickly, and it is definitely a seller’s market, so you might sell your house in a hot second, but if your place is more rural, expensive, or unique, you’ll probably wait longer.

Do you have a home that has been languishing on the market for a long time compared to other properties in your area? This may be due to being overpriced, having condition issues, or becoming “stale” compared to newer listings. Don’t wait – discuss your timeframe with your Realtor® ASAP!

How long does it take to close after we receive an offer?

Answer: 30-60 days

Currently (nationwide), there’s an average of 50 days between when buyers apply for financing and when they get approved and can close on a home, and that timeframe is not uncommon in our area. Yes, that’s a long time, especially if you’re selling and eager to get on with it. But buyers and mortgage companies need to do their due diligence—and you certainly don’t want any last-minute surprises before the buyer takes possession. A dearth of qualified appraisers and a very busy market are definitely adding to that challenge. Closings fail for a number of reasons, like contingencies (perhaps the buyer’s home didn’t sell, or the bank rejected the loan). Whatever you do, don’t refuse or wait too long to fix issues that arise during inspection (assuming, of course, you agreed to fix them). Final walk-through surprises can delay closing even longer.

How long before I get paid?

Answer: 0 days!

Here’s good news: Your money should be available immediately after the transaction is recorded with the County. Cash is typically disbursed by the escrow company, which will wire the money to your bank account or cut a check on closing day with little to no lag time. Make sure to check with your attorney or escrow closer, though—they will be able to provide specific details on the process for your specific sale. And remember – there is often a day or two lapse between when documents are signed and the County actually records and closes your transaction. Recording numbers from the County are the seal on a deal successfully closed!

How long do I have to move out?

Answer: 0 days, except by special agreement

Typically, sellers are expected to move out no later than 9:00 p.m. the day they close on the home so the new buyers can move in as soon as the transaction is recorded. Many people move out in advance of the close (or at the very least earlier on the day of closing), but if you need more time, you may be able to negotiate a rent-back agreement, which allows the new buyers to essentially become your landlords for a brief period of time while you find a new place to live. But considering how long the home-selling process takes, odds are you’ll be chomping at the bit to get out and move on!

Questions? As always, feel free to ask. I am here and happy to help!

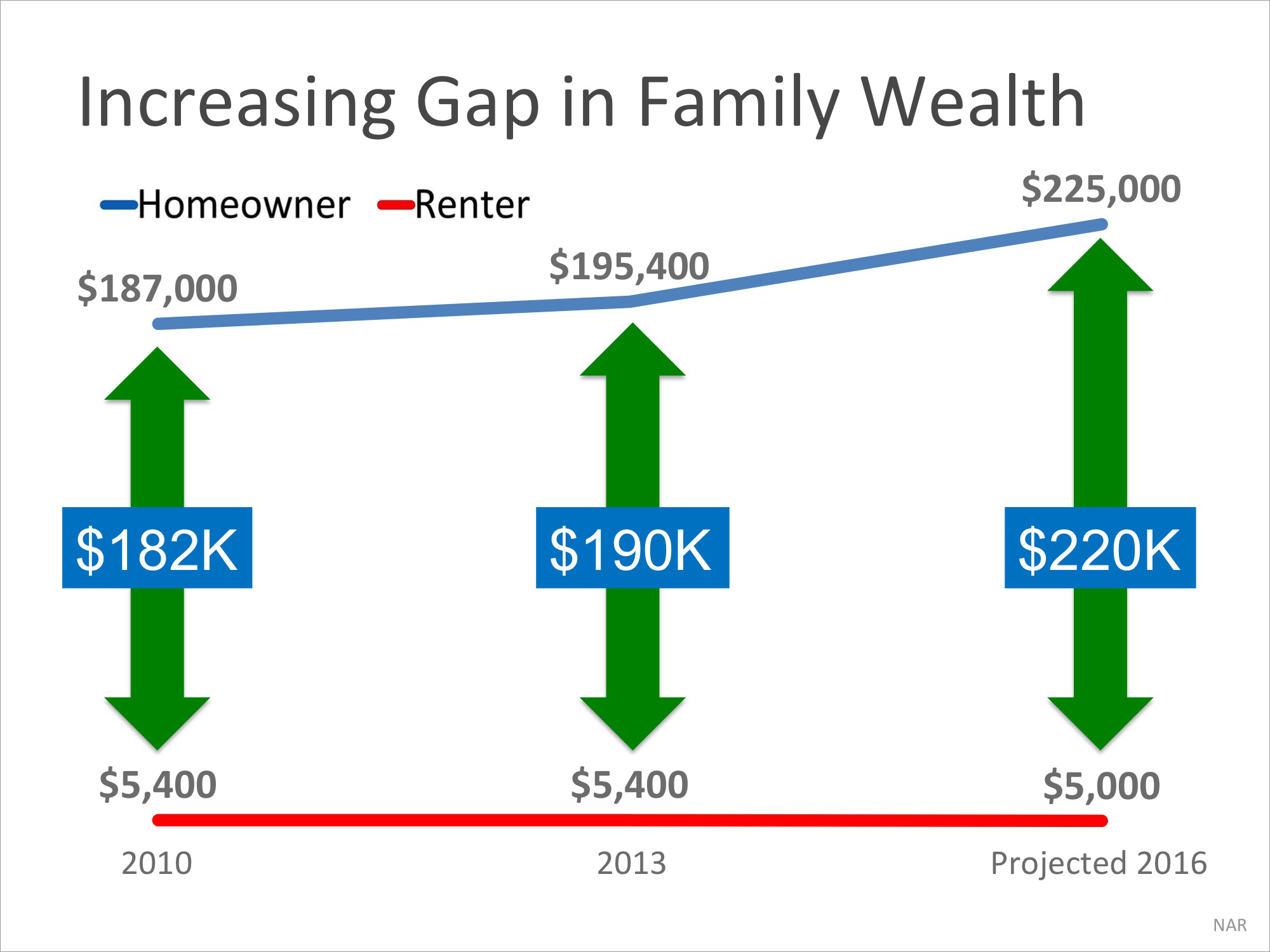

Every three years, the Federal Reserve conducts a Survey of Consumer Finances in which they collect data across all economic and social groups. The latest survey, which includes data from 2010-2013, reports that a homeowner’s net worth is 36 times greater than that of a renter ($194,500 vs. $5,400).

In a Forbesarticle, the National Association of Realtors’ (NAR) Chief Economist Lawrence Yun predicts that by the end of 2016, the net worth gap will widen even further to 45 times greater. Federal Reserve Survey data is not yet in for the 2013-2016 timeframe, but based upon economic recovery and increases in home equity in the past three years, Yun’s prediction appears to be on target.

The graph below demonstrates the results of the last two Federal Reserve studies and Yun’s prediction (note the reduction in savings as well as the increase in home values over time):

Put Your Housing Cost to Work for You

As I’ve mentioned in past blogs, simply put, homeownership is a form of ‘forced savings.’ Every time you pay your mortgage, you are contributing to your net worth. Every time you pay your rent, you are contributing to your landlord’s net worth. The requirement to make your mortgage payment each month ensures your funds won’t be diverted away from your home equity savings plan. And for those who intend to occupy a residence for more than a year or two, it really is that simple.

The latestNational Housing Pulse Survey from NAR reveals that 85% of consumers believe that purchasing a home is a good financial decision. Yun comments:

“Though there will always be discussion about whether to buy or rent, or whether the stock market offers a bigger return than real estate, the reality is that homeowners steadily build wealth. The simplest math shouldn’t be overlooked.”

Bottom Line

Owning a home, building wealth, leaving a legacy for the future is at the heart of the American dream. If you are interested in finding out if you could put your housing cost to work for you by purchasing a home instead of renting, let’s get together and evaluate your ability to buy today. And, as always, if you have questions please don’t hesitate to let me know. I’m here to help!

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link