Most of us share a belief that there are some social advantages to home ownership. However, some people question the financial benefits of owning a home. When questioning the assumptions, we can take advantage of three recent studies to shed some light on the issue.

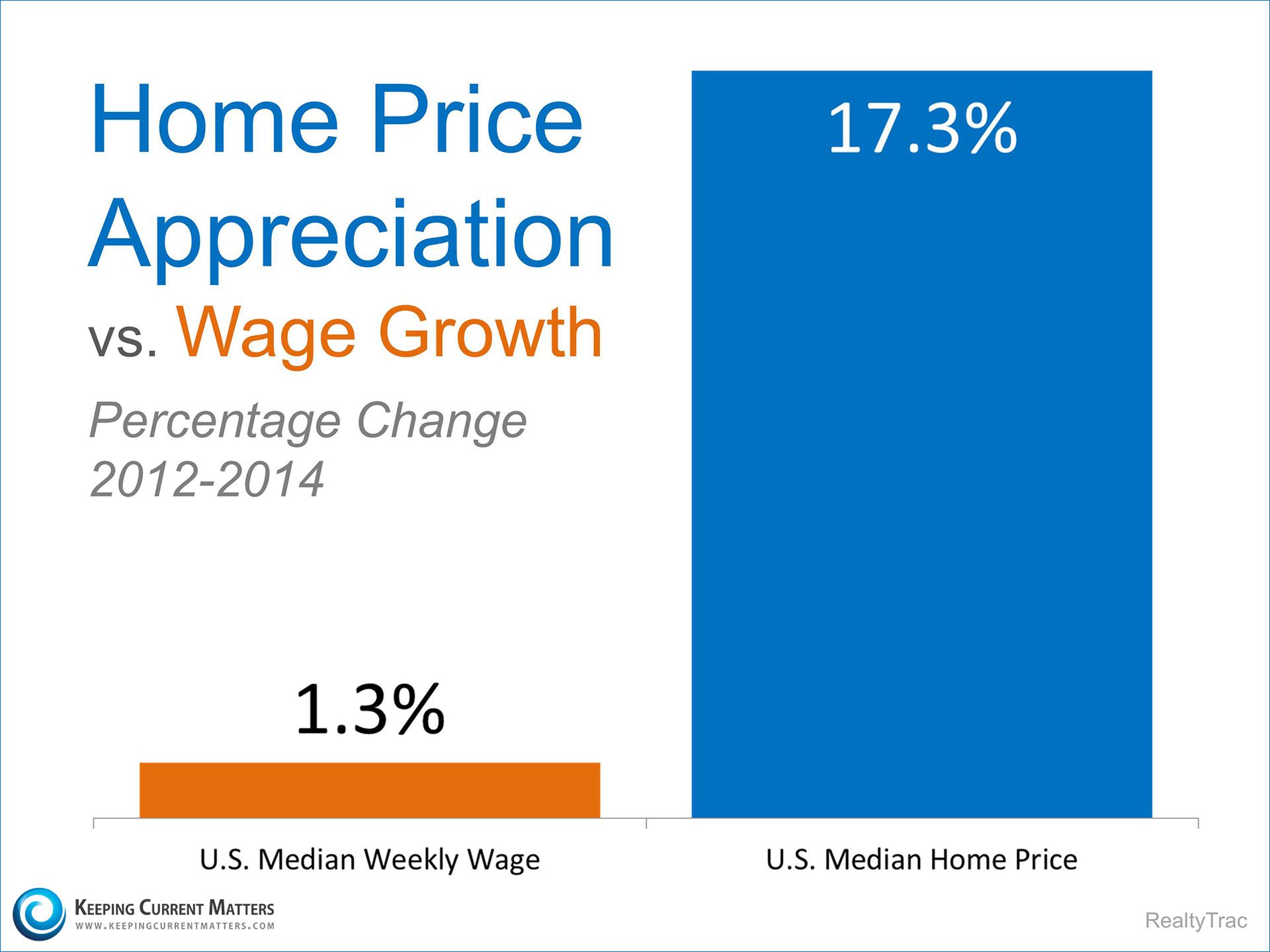

RealtyTrac recently released a report comparing home price appreciation to wage growth over the last two years. The study revealed that home price appreciation has outpaced wage growth in 76% of U.S. housing markets during that same time period. Put simply, that means our buying power is decreasing over time. But by how much? Here is a graph showing their findings:

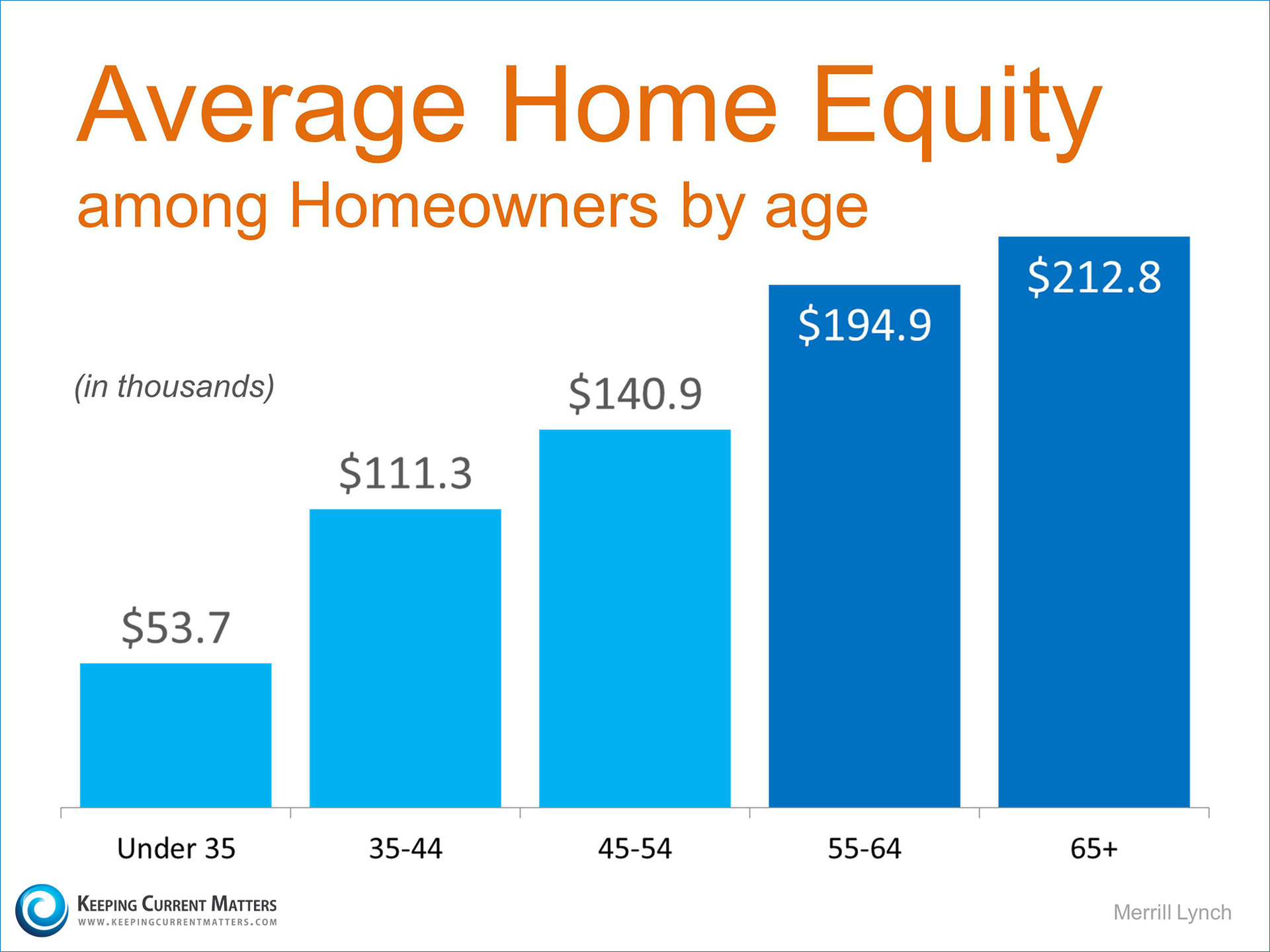

This is a huge gap, a 16% deviation over 24 months in three-quarters of the U.S. housing markets. In a previous blog we discussed the importance of home value appreciation in determining the net wealth of most American families. Merrill Lynch just issued a report covering the issue. Their findings are shown here:

On average, putting the benefits of home value appreciation to work as early in your life as possible makes financial sense in today's market when looking at wealth building.

But, does it make sense to buy now?

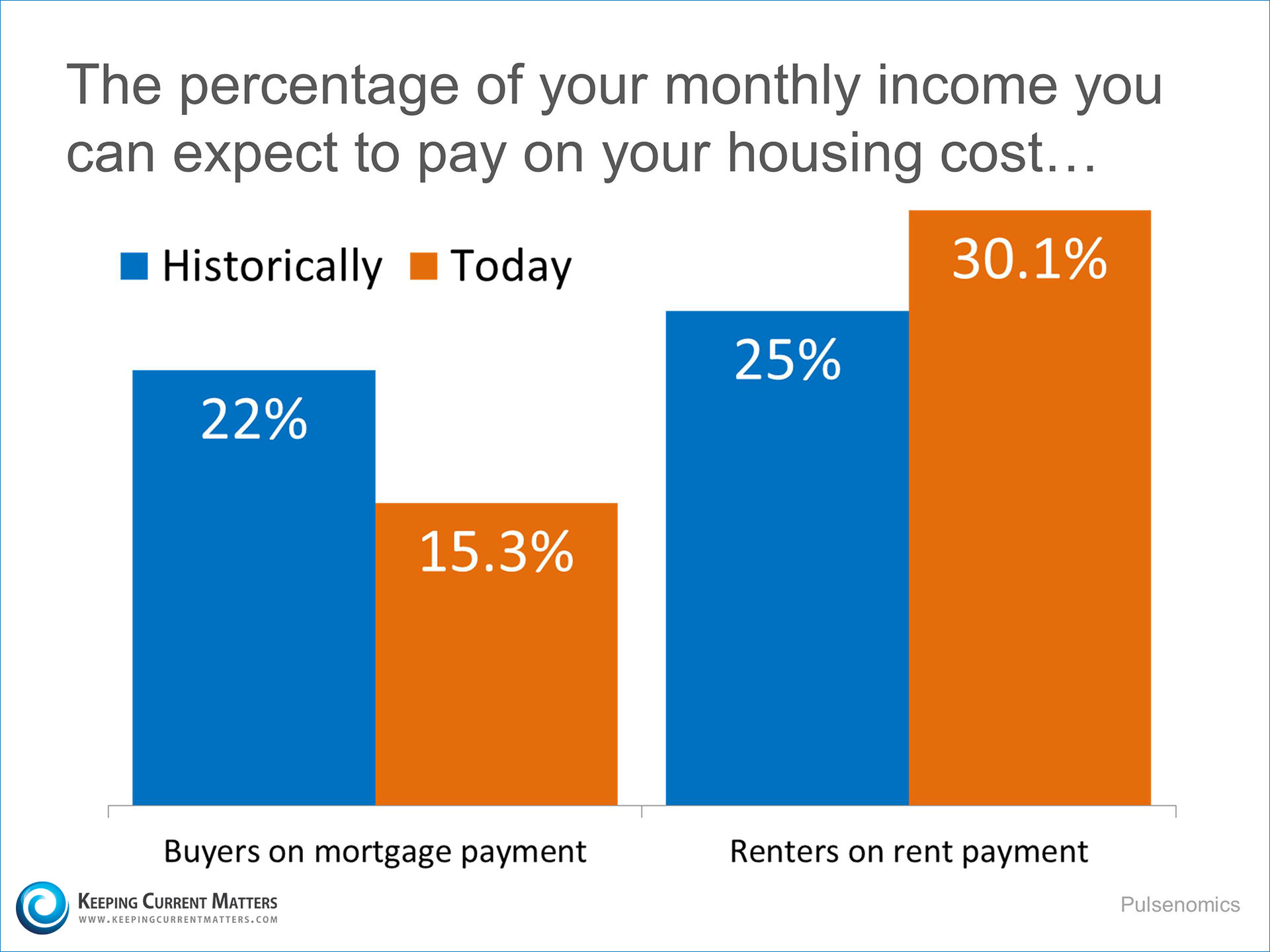

The survey company Pulsenomics just issued their findings on the cost of owning versus the cost of renting. They compared historical averages to the cost you can expect to pay today.

While the cost of buying is far below historical averages, renting in today's market is another story. Are you a renter or first-time home buyer interested in knowing more about the value of home ownership as well as the possibilities open to you? Let's get together and talk!

If you are debating purchasing a home right now, you may be getting a lot of advice. Though your friends and family will no doubt have your best interests at heart, they may not be fully aware of your needs and what is currently happening in real estate. Before you make that decision, let’s look at whether or not now is actually a good time for you to buy a home.

There are 3 questions you should ask before purchasing in today’s market:

1. Why am I buying a home in the first place?

This truly is the most important question to answer, and one you should give serious thought. Forget your finances for a minute. Why did you even begin to consider purchasing a home? For most people, the reason has nothing to do with finances. This is most often a heart decision, not a head decision.

A study by the Joint Center for Housing Studies at Harvard University reveals that the four major reasons people buy a home have nothing to do with money:

A home is a good place to raise children and for them to get a good education

A home is a place where you and your family feel safe

Your own home would provide more space for you and your family

Your own home allows you control of that space

What non-financial or "heart" benefits will you and your family derive from owning a home? The answer to that question should be the driving reason behind your decision to purchase or not. I suggest you write down your reasons and keep them in front of you before, during, and after your decision-making process. They will help guide you in deciding not only when to buy, but also where and what will meet your needs.

2. Where are home values headed?

When looking at future housing values, Home Price Expectation Survey provides a fair assessment. Every quarter, Pulsenomics surveys a nationwide panel of over 100 economists, real estate experts and investment & market strategists about where prices are headed over the next five years. They then average the projections of all 100+ experts into a single number.

Here is what the experts projected in the latest survey:

Home values will appreciate by 4.4% in 2015

The cumulative appreciation will be 19.3% by 2019

Even the experts making up the most bearish quartile of the survey still are projecting a cumulative appreciation of over 11.7% by 2019

This information should be factored into your "head" decision. Does the prospect of home appreciation, particularly at the conservative or bearish level, factor appropriately into your financial plans?

3. Where are mortgage interest rates headed?

A buyer must be concerned about more than just prices. The ‘long term cost’ of a home can be dramatically impacted by an increase in mortgage rates.

The Mortgage Bankers Association (MBA), the National Association of Realtors andFreddie Mac have all projected that mortgage interest rates will increase by approximately one full percentage over the next twelve months. How will an increase, if it happens, affect your future ability to buy and your long-term ability to pay for a home? Is now a better time for you, over time, than a year or two from now?

Bottom Line

Only you and your family can know for certain the right time to purchase a home. Answering these questions will help you make that decision. And if I can help you by providing more information, please don't hesitate to let me know!

I believe that as most of us grow and up and grow our families, we have a vision of leaving a legacy of some kind for future generations. That legacy often includes plans for providing some kind of monetary security in addition to other positive contributions we might make. That vision isn't always easy to map or achieve, however.

Matthew Rognlie, from the Department of Economics at MIT, recently released a paper: Deciphering the Fall and Rise in the Net Capital Share. Although the report itself is fairly complex, when distilled down one of the major findings of the report is that homeownership is and has been for the last fifty years a major component to family wealth.

An article on the study in The Economist notes one of the findings of the study:

“The return on non-housing wealth, in fact, has been remarkably stable since 1970. Instead, surging house prices are almost entirely responsible for growing returns on capital.”

This came as no surprise, as the Federal Reserve reported that the net worth of families that own their own home is 36 times greater than that of families that rent. Every three years the Federal Reserve conducts a Survey of Consumer Finances in which they collect data across all economic and social groups. Some of the findings revealed in their report include:

The average American family has a net worth of $81,200

Of that net worth, 61.4% ($49,856) of it is in home equity

A homeowner’s net worth is over 36 times greater than that of a renter

The average homeowner has a net worth of $194,500 while the average net worth of a renter is $5,400

Bottom Line

HousingWire’s Senior Financial Reporter, Trey Garrison, summed it up well in his reporting on Rognlie’s study:

“Homeownership has consistently created generational wealth more reliably, and more ‘democratically’, than any other asset class. And it does so in a manner entirely ancillary to its primary purpose of giving you a place to lay your head and keep your stuff.”

Interested in leaving a legacy for future generations? It appears that the best foundation you can have just may be home ownership!

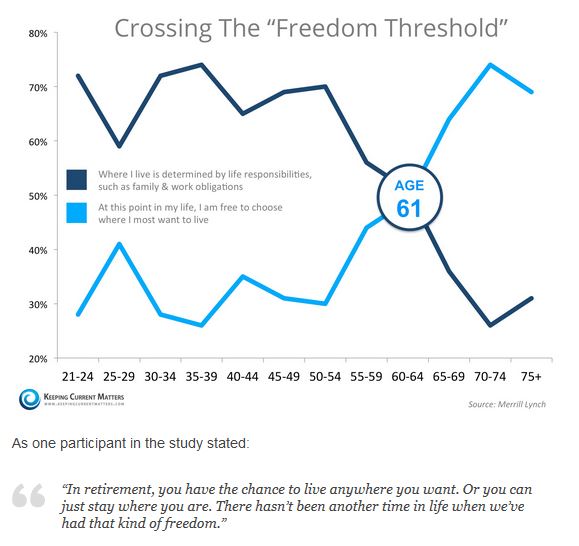

I ran across that phrase recently – "Crossing the Freedom Threshold" – and it intrigued me enough to pursue it further. What I discovered is that it describes a time in life where the place that we live is no longer dictated by responsibility but is based solely on choice. What a great phrase to describe a wonderful concept!

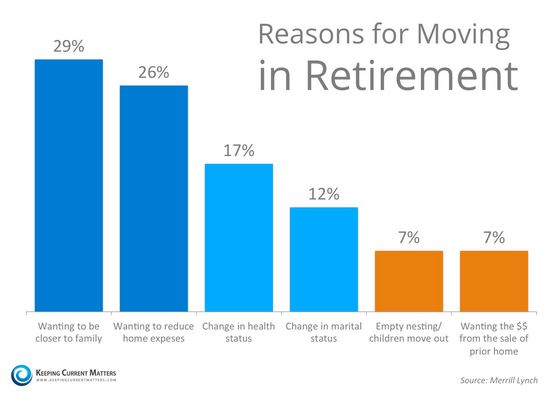

Within the next five years, Baby Boomers are projected to have the largest household growth of any other generation during that same time period according to the Joint Center for Housing Studies of Harvard.In Merrill Lynch’s latest study, “Home in Retirement: More Freedom, New Choices,” they surveyed nearly 6,000 adults ages 21 and older about housing.The study disclosed that throughout our lives there are often responsibilities that dictate where we live. Whether being in the best school district for our children, being close to our jobs, or some other factor is preventing a move, the study found that there is a substantial shift that takes place at age 61. The study referred to that shift as "Crossing the Freedom Threshold."

According to the study, “an estimated 4.2 million retirees moved into a new home last year alone.” Two-thirds of retirees say that they are likely to move at least once during retirement.The top reason to relocate cited was “wanting to be closer to family” at 29%, a close second was “wanting to reduce home expenses”.

Not Every Baby Boomer Downsizes

There is a common misconception that as retirees find themselves with fewer children at home they will instantly desire a smaller home to maintain. While that may be the case for half of those surveyed, the study found surprisingly enough that three in ten decide to actually upsize to a larger home.Some choose to buy a home in a desirable destination with extra space for large family vacations, reunions, extended visits, or to allow other family members to move in with them.

"Retirees often find their homes become places for family to come together and reconnect, particularly during holidays or summer vacations."

Bottom Line

Regardless of where you are in life, if your housing needs have changed or are about to change, I'd love to meet with you to explore your options and discuss your next steps!

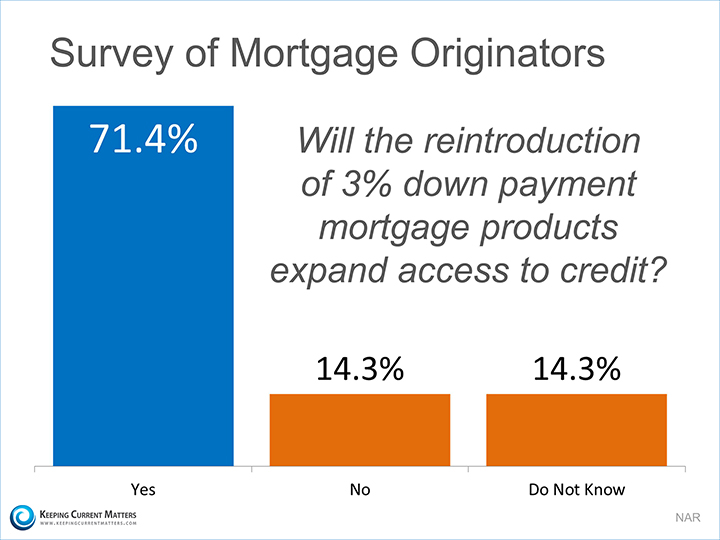

Today, Freddie Mac is scheduled to start buying mortgages with down payments of only three percent – the first time down payments have been this low on Freddie Mac loans in nearly five years. The program is called Freddie Mac Home Possible AdvantageSM.

What is the Impact?

In a recent copy of the publication "Executive Perspectives," Dave Lowman EVP, Single-Family Business Freddie Mac, explained the potential impact this program will have on the housing market:

“There's a new reason Realtors and lenders may expect more qualified borrowers at the closing table during this spring's home buying season. In addition to low mortgage rates and rising job growth, the down payment hurdle is starting to shrink for creditworthy borrowers, including first-time homebuyers.”

And the mortgage industry appears to agree with Mr. Lowman. In a recent survey of mortgage originators by the National Association of Realtors (NAR), it was revealed that the majority of loan officers believe the move to a lower down payment will increase access to mortgage credit for many would-be homeowners. The chart below illustrates that survey’s findings:

And What is the Bottom Line?

Many potential buyers are “ready and willing” to buy a home but have been afraid they may not be “able” because of a lack of adequate savings for a down payment. Given this new move on the part of Freddie Mac, that hurdle may be just that much easier to overcome. Do you have questions? Feel free to ask, and I will be more than happy to help you understand what the new rules may mean to you!

Real estate professionals are engaged in an interesting profession. We interact all the time with individuals unfamiliar to us. We go out, most often alone, to show homes and properties to people we may have never met (not wise, I know, but true). And the majority of the time we are safe. But on occasion we are not, and with all the advances in technology it is good to see some of the options coming available to help us feel and be more secure.

First of all, we should ALL require new clients to come into our offices to meet face-to-face before going out to preview properties. But we don’t always do that. And we should also always require prospects to leave a copy of their driver’s license and their license plate number with our office staff. But we don’t. And most often we don’t do these things because requiring them is inconvenient for the client, but that’s another topic of conversation. Even if we take these basic steps, we may still be at risk. So what else can we do?

One of the newer options available to us is wearable technology, alarm systems or distress beacons built into jewelry that can be activated discreetly and easily. Cuff links, necklaces/pendants, bracelets, and more are available that are both stylish and functional. The companies Cuff, First Sign, and Stiletto are all actively engaged in this market with products that can deliver distress signals as well as do more, and I encourage you to visit their websites to learn more about them.

Another option is using an app to remotely verify the identity of the individual you are planning on meeting. This can be done via cell phone, but the turnaround time for verification can be 30 minutes or more, so using this app needs to be done in advance of an actual meeting. You can find more information through the company Secure Show.

In addition, there are applications that can alert others when you are in distress and they include those from Guardly, SOS-StaySafe, bSafe, Emergensee, Watch Over Me, and Agents Armor among others. These apps work in a variety of ways – some by shaking your phone, some by pressing a single button, some that allow audio or video feed, some that provide GPS tracking, and more. The wide range of options should provide everyone with a solution that will work for them.

It’s good to know we have options for personal safety, and it’s even better when we can share what we know with others who can benefit. These companies and their products benefit not only realtors but they can also benefit children, students, people working odd hours or those working in risky neighborhoods. If you know someone who might be able to use one of these technologies, will you please share?

I’m not much of one for ripping articles out of magazines, but a few months ago I tore an editorial out of an industry publication because there were sentiments in it that resonated with me. I kept the article, and today I am sharing a few of the author’s insights – as well as my own – with you.

The following question was asked of Steve Brown, 2014 President of the National Association of Realtors. “Isn’t the real estate industry just like any other business? Don’t we have a product to sell? Isn’t the industry based on profit and loss and market share just like any other business?”

I am joining Steve Brown in his response, which essentially was, “No…The answer to your question is a resounding no!” As a Real Estate Professional and a businessperson, of course there are business models that underlie how I perform. But those models do not address the “why” of what I do, and I believe it is in the “why” that real estate is differentiated.

In 1924, the National Association of Realtors rewrote the preamble to its Code of Ethics, and the new Code begins, “Under all is the land.” Following that phrase, the Code of Ethics sets out the business as well as social responsibilities of Realtors. The Code recognizes that land carries intrinsic value, whether it is used for residential, commercial, institutional, farming, or other purposes. Real estate professionals are charged with overseeing the transactions that safeguard the land’s value. In addition, however, land and its ownership carry social and emotional meaning for most.

Land ownership expresses value in many ways. People dream of places to make beautiful, places where they can give physical expression to personal values, places where they can live out a specific lifestyle or conduct a profitable business. They also dream of security, both financial and physical. And for many, the ownership of land is an expression of accomplishment for the world to see and appreciate. Property ownership is a physical expression of deeply embedded thoughts and feelings, and for many it is also one of the most significant financial investments they will make in their lifetime.

So is real estate a product like any other? No, it’s not. It is finite. It can be nurtured, or it can be rendered useless. It is tied to hearts, minds, cultures, and pocketbooks. Many of the thoughts and feelings tied up in land ownership are similar across a wide range of boundaries around the globe. There is nothing else like it, and working in the real estate industry is a job like no other. And for me, it is because it is NOT “business as usual” that I am involved. I love working to safeguard the land and its value as well as the social, emotional and financial investments people make. I work in this industry because I truly love being engaged in ALL the facets of helping people make their real estate dreams come true!

I’ve blogged a bit recently about the Seahawks, about wins and losses, and about my hopes for the new year. All of this comes with some contemplation about mistakes I’ve made in the past, both in business and in my personal life. So as I look back over the recent months and years, and before I turn my focus totally toward what is ahead of me, I thought I’d share with you what I consider three of the bigger mistakes I’ve made not only in business but in life in general.

My first big mistake is one I’ve vowed to overcome by learning from the Seahawks, and that one is giving up too easily. In the past I have given up before I have truly been defeated. That one really bugs me, and I am hereby vowing to remember the following:

Every attempt at something is a way to learn how to do it better next time

It takes many attempts to achieve one success

The most meaningful things are not easy to achieve

I don’t know how meaningful my success might be until I actually accomplish

I may be failing because I haven’t tried the right thing yet

Tenacity matters more than talent

My past does not determine my future

My second big mistake on this list is spreading myself too thin. I have allowed myself to be influenced by a culture that values busyness over enjoyment and by people that place productivity over relationships. I know individuals who pride themselves on how little sleep they get in their pursuit of busyness, and I bet you do, too. But I am no longer going to allow those people and those attitudes to influence me, and I am hereby vowing to remember the following:

Overcommitting myself causes stress overload, and stress overload can cause lack of sleep, fatigue, poor eating habits, mood swings, forgetfulness, and even illness

Stress overload can lead to a breakdown, and any breakdown takes away my freedom of choice

My to-do list is incomplete without down time, without me time, without time for the little things as well as time for others

It is okay – in fact it is better than okay – to just say “no” to anything that overcommits me in an unhealthy way

And my third big mistake (at least on this list) is being afraid, of giving in to fears real and imagined, fears both big and small. I am not a courageous person by nature, but I want to live life with some form of bravery and daring. To do that, I need to overcome the fears that hold me back, so I am hereby vowing to remember the following:

Most things that frighten me aren’t real, they are imagined, and the fact that they live only in my imagination means they are not true

I don’t want my life to be governed by things that are not true

When afraid, it is most often better to do something than to do nothing at all

Setting small goals or taking small steps is an easy way to start to overcome my fears

I have a choice about how I react in any given situation

I can always choose to focus on the positive

That’s it. Those are the things I am vowing to remember in the days and weeks and even years to come. What about you? What’s holding you back, and what do you vow to do about it?

Tonight I was reading some notes from John Burns (John Burns Real Estate Consulting) and contemplating how his thoughts apply to our market here in the Poulsbo area. We currently have several hundred new housing starts either under construction or planned for construction in the very near future. I have been wondering about the builders and developers who are going to be investing in and marketing these homes, and I have been wondering who will be occupying them. Here are some of John Burns’ thoughts on what builders should be focusing on nationwide. I am excited to see how it all plays out in my neighborhood. Number 3 is a definite need in our area! Do you agree?

1. Less move-up housing

“Many of those born in the 1970s bought their first home 10+/- years ago and thus are far less likely to have sufficient equity to move,” Burns said. “They are also more likely to have gone through foreclosure, which has a marginally positive housing demand element to it, as some will return to homeownership soon. Not only are there fewer traditional move-up households, but a high percentage of them are unable to move.”

2. More luxury housing

“Luxury home buying typically occurs when buyers reach their years of peak earning and net worth,” Burns said. “The U.S. currently has more people in this group, aged 46-60, than ever before, and they have more income (two careers) and less expenses (fewer kids) than any generation before them. Compared to prior generations, this group is loaded.”

3. More retiree housing

“Eight million more people will turn 65 over the next 10 years than the last 10 years, and more of them than ever before plan to move, according to our Consumer Insights survey,” Burns said. “This creates opportunities in all regions and at all price points, as the demand drivers are no longer solely golf courses in sunny states. Proximity to kids and grandkids, as well as entertainment, and health and wellness are just a few of the main success drivers we see over and over.”

4. More entry-level housing, but not yet

“While entry-level buyers are financially challenged, the number of people is so large and the desire to own so high that many entry-level buyers will emerge over the next decade, especially if mortgage rates and down payment requirements stay low,” Burns said. “While most will buy resale homes for affordability reasons, a small percentage of a large number will still translate to strong new home demand.”

Two weeks ago I wrote a post concerning the Seahawks NFC Championship win and how much I love our team in general. Last night I watched the Super Bowl game with as much anticipation and excitement as any Seahawks fan. I was decked out in my team apparel, and I was excited to be a “12.” I was a dedicated 12 yesterday, and today I still am!

Once again it wasn’t our very best game. Both teams brought skill, spirit, and strength to the game. Both were also lucky at times. We had to really fight to gain ground against the Patriots, but, as we often do, we took the lead in the second half. Then, with only seconds remaining on the clock and within three yards of the goal line, Super Bowl victory seemed within our grasp. In that moment a decision had to be made whether to pass the ball and hope it reached its intended receiver or whether to hand off the ball and hope Marshawn Lynch successfully carried it across the goal line.

I think everyone watching the game expected we would go “Beast Mode” and give Lynch the opportunity to carry the ball across the line. I know I did. I am sure I was as shocked and surprised as everyone else when we chose to pass the ball and the pass was intercepted. It’s hard to go from Super Bowl Champions to second place in the blink of an eye like that, and yet it happens. No matter what we did, it could have gone either way. Unfortunately, it ended with that interception and the events that followed.

I didn’t like the way the game ended. I didn't like the fact that we lost. To quote Russell Wilson, I hate losing. I didn’t care for the unsportsmanlike conduct – the pants-dropping gesture or the punch thrown or the brawl in the end zone and the penalties incurred. I think the Hawks can and should be better than that. But as a team, I still love them! I love the fact that the Seahawks didn’t give up. They played as a team, they played through pain and injuries, and they played to win. I know, they are paid well to play well, and so they should. But they have something special both on and off the field, and I love them for all that they do. I love them as a team, I love the players for their commitments to causes outside of themselves, and I love them for the men and leaders they are as well as those they hope to be when football is a part of their past.

I not only love the Seahawks, I love business. There's a connection between the two – strategy, team effort, planning, purpose. I hope to learn lessons from this game that I can apply to my business as well as others’. And, as I said before, when it looks like I’m not winning I hope I don’t lose my vision. I hope I don’t make excuses, and I hope I don’t give up. I intend to push through and play well, and I hope you do, too. And speaking of winning, of course there’s always next year!

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link