CoreLogic recently released their 2015 2nd Quarter Equity Report which revealed that 759,000 properties had regained equity in the last quarter. That means that 91% of all mortgaged properties (approximately 45.9 million) are now in a positive equity position. Anand Nallathambi, president and CEO of CoreLogic, reported:

“For much of the country, the negative equity epidemic is lifting. The biggest reason for this improvement has been the relentless rise in home prices over the past three years which reflects increasing money flows into housing and a lack of housing stock in many markets.”

Obviously, this is great news for the financial situation of many homeowners.

But, do they realize their equity position has changed?

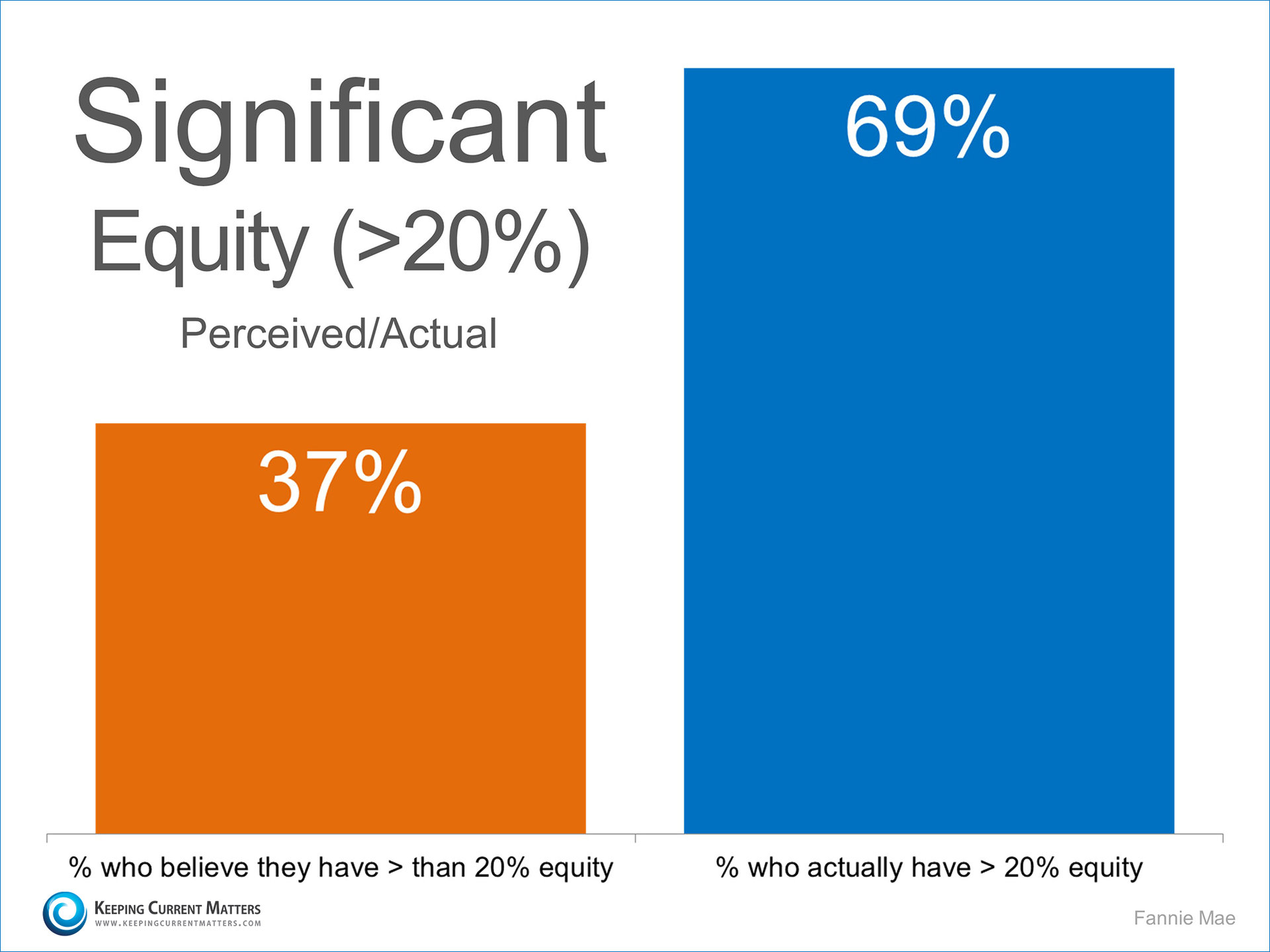

A recent study by Fannie Mae suggests that many homeowners are unaware that their equity position has changed…in some cases dramatically. For example, their study showed that 23% of Americans still believe their home is in a negative equity position when, in actuality, only 9% of homes are in that position.

The study also revealed that, though 69% of homes had “significant equity” (greater than 20%), only 37% of Americans realize it.

Surprisingly, this means that 32% of Americans with a mortgage fail to realize the opportune situation they are in. With a sizeable equity position, many homeowners could easily transition into a housing situation that better meets their current needs (either by moving to a larger home, upgrading their current home, or downsizing).

Fannie Mae spoke out on this issue in their report:

“Homeowners who underestimate their homes’ values not only underestimate their home equity, they also likely underestimate 1) how large a down payment they could make with their home equity, 2) their chances of qualifying for mortgages, and, therefore, 3) their opportunities for selling their current homes and for buying different homes.”

Bottom Line

Every homeowner should be aware of the true equity in their house and also realize the opportunities that go along with it. If you are unsure of the savings you currently have built up in your home, feel free to ask me to help you ascertain that number. You may be pleasantly surprised. And, as always, if you have other questions or if there is another way I can help with your real estate needs, please don't hesitate to ask!

Are you on the fence right now as to whether or not it is the right time to buy? You will often hear homeownership being promoted over renting when a family is ready, willing and able to purchase. (See my blog from August 31 regarding building wealth.) There are both financial and non-financial benefits to owning a home of your own, and homeownership is still considered a major component of living the American Dream. Based on the headlines included below, many news outlets agreed with owning rather than renting after they reviewed a recent report from the Harvard Joint Center for Housing Studies and Enterprise Community Partners.

The report states that the number of households spending 50% or more of their income on rent is expected to rise by over ten percent in the next decade. About this group, they say:

"In a baseline scenario where both rents and incomes grow in line with inflation (set at 2 percent), we find that demographic trends alone would raise the number of severely burdened renter households by 11 percent from an estimated 11.8 million in 2015 to 13.1 million in 2025."

That is a possible 13.1 million households in the next 10 years that will be paying 50% or more of their income on rent. They concluded:

“Overall, this white paper projects a fairly bleak picture of severe renter burdens across the US for the coming decade.”

What do other experts think of the report? You can tell by the headlines they chose to introduce their stories:

“Renters, get ready to take it on the chin” – CNBC

“The Rent Crisis Is About to Get a Lot Worse” – Bloomberg Business

“Renters Will Continue to Struggle for the Next Decade” – World Street Journal

“Why the renting crisis could be about to get a lot worse” – Fortune Magazine

“Soaring rents are a problem that will only get worse” – Business Insider

“High rents are here to stay” – The Real Deal

Bottom Line

If you are thinking about buying a home and are financially positioned to do so, sooner may be better rather than later. The rental market is tight and is expected to remain that way, rents will continue to rise over time, and so will the costs related to homeownership. Confused as to what to do? The best thing may be to sit down with a real estate professional to discuss your options. And, as always, if I can help in any way please don't hesitate to ask!

In today's market, with homes selling quickly and prices rising, some homeowners might consider trying to sell their home on their own, known in the industry as a For Sale by Owner (FSBO). There are several reasons this might not be a good idea for the vast majority of sellers.

Here are five reasons, highlighted by a personal experience just this week:

1. Negotiations are complex

Here is a list of some of the people with whom you must be prepared to negotiate if you decide to engage in a For Sale By Owner transaction:

The buyer, who wants the best deal possible

The buyer’s agent, who solely represents the best interest of the buyer (and expects a commission for bringing a ready, willing and able buyer)

The buyer’s attorney (in some parts of the country or if there is no buyer's agent)

The home inspector, who work for the buyer and will almost always find some problems with the house

The appraiser, if there is a question of value

The title company, if there are any issues exposed by the title search

The escrow company, if there are questions regarding buyer's and seller's debits and credits or contract items

Are you prepared to deal with the stress and possible expense of self-representation in these areas? Are you prepared to lose a sale if negotiations break down? Are you prepared to devote time and attention to each of these areas in order to close a sale?

2. Exposure to Prospective Purchasers

Recent studies have shown that 88% of buyers search online for a home. That is in comparison to only 21% looking at print newspaper ads. Most real estate agents understand the market and have a strong and comprehensive strategy to promote the sale of your home. Do you?

Just last week I had a buyer ask me to show her a property that was listed FSBO. I performed an online search for the property by address as well as searching the MLS. I could find no record of the property being for sale. This week I had another individual ask me about the same property, and again my search turned up nothing. However, the owner believes her home is being given the same exposure as if she had listed it with a real estate firm. Online exposure, professional photographs and staging, Broker's Tours, open houses, signage, print ads, word of mouth – all of these, routinely provided by a competent listing agent – are necessary to generate the exposure your home needs in order to sell in a timely manner for the best price.

3. Results Come from the Internet

Where do buyers find the home they actually purchased?

43% on the internet

9% from a yard sign

1% from newspaper

The days of selling your house by just putting up a sign and putting it in the paper are long gone. Having a strong internet strategy is crucial, and most individuals don't have the expertise or time necessary to create and maintain such a presence. Do you have access to posting your home on your personal website, your company site, and sites such as Zillow, Trulia, Redfin, Realtor.com, Yahoo Real Estate and more? Without that exposure, and without the staging, photographs, and descriptions to support that online presence, you are bypassing your most valuable audience.

4. FSBOing has Become More and More Difficult

The paperwork involved in selling and buying a home has increased dramatically as industry disclosures and regulations have become mandatory. This is one of the reasons that the percentage of people FSBOing has dropped from 19% to 9% over the last 20+ years. Do you know the laws that govern disclosure and what information you must share with prospective buyers? Are you up to date on when and how a buyer is able to walk away from a transaction and still retain their earnest money? Are you aware of the privacy laws that govern when and how you can (or cannot) use cameras or audio feed in your home? Do you have a strategy for making keys available and showing your home convenient for all concerned? The process is complex and continues to become more so every day.

5. You Net More Money when Using an Agent

Many homeowners believe that they will save the real estate commission by selling on their own. However, saving a commission isn't the measurement of success in selling a home. Selling your home for the right price in a timely manner is the true measurement of success, and determining market value is one of the most strategic aspects of listing a home for sale. Having access to the most current and reliable data and being provided a Comparative Market Analysis for your home is one of the benefits of using a listing agent. If you undervalue your home and sell it too quickly, then you have left money on the table. If you overvalue your home and it sits for weeks and has to be marked down before finding a buyer, you have lost both time and money. Using a professional to get it right from the beginning will bring you the best value for your home.

Studies have shown that the typical house sold by the homeowner sells for $208,000 while the typical house sold by an agent sells for $235,000. This doesn’t mean that an agent can get $27,000 more for your home, as studies have shown that people are more likely to FSBO in markets with lower price points. However, it does show that selling on your own might not make sense.

Bottom Line

Before you decide to take on the challenges of selling your house on your own, sit with a real estate professional in your marketplace and see what they have to offer. Your consultation should be free, and you might find you will gain more than you think by listing with an agent. And, as always, if I can answer any questions for you, please don't hesitate to ask!

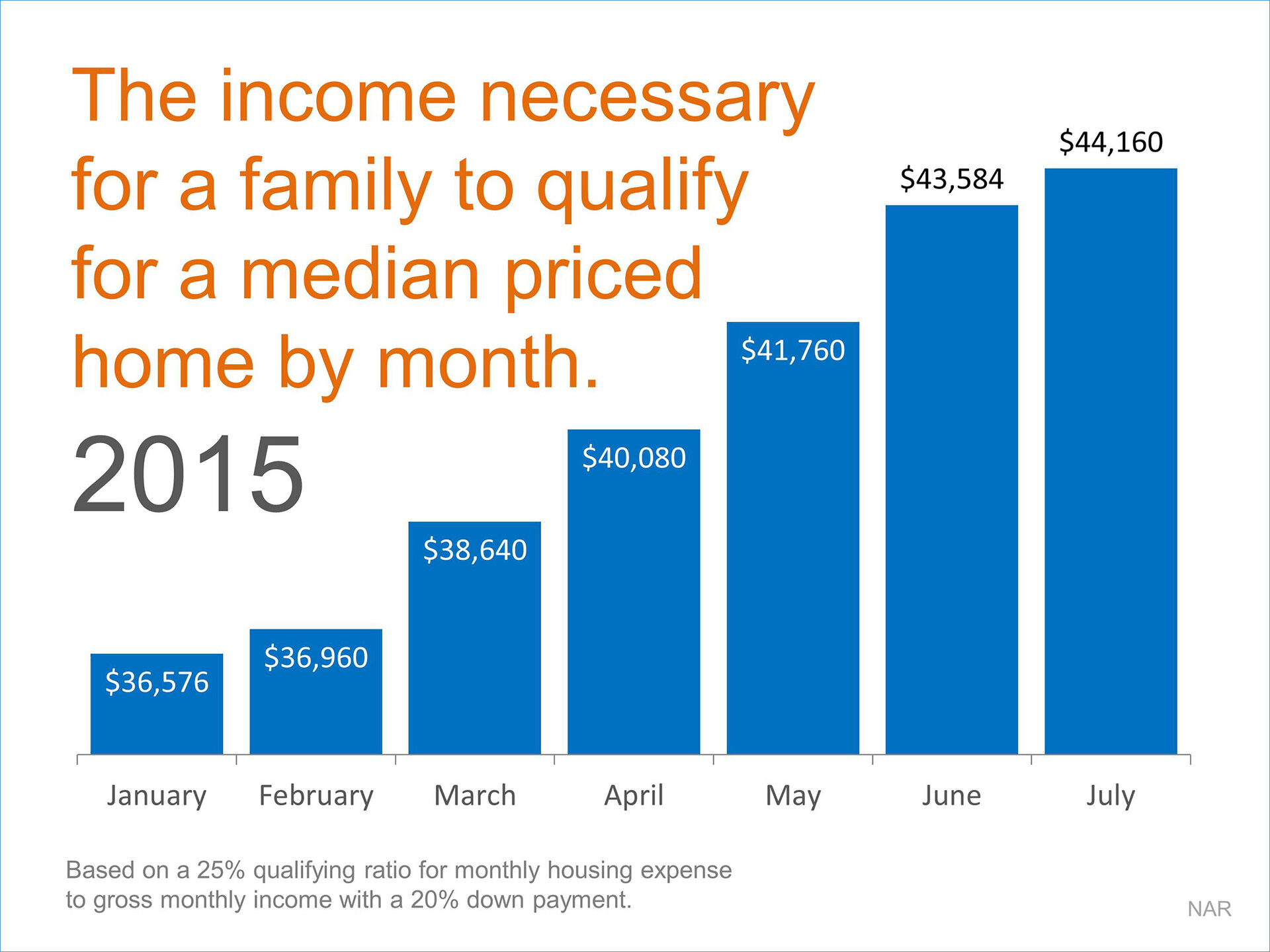

The National Association of Realtors (NAR) recently released their July edition of the Housing Affordability Index. The Index measures whether or not a typical family earns enough income to qualify for a mortgage loan on a typical home at the national level based on the most recent price and income data. This information is based upon national figures but is adjustable to our area by modifying the median sales price for the neighborhood in which you are interested.

NAR looks at the monthly mortgage payment (principal & interest) which is determined by the median sales price and mortgage interest rate at the time. With that information, NAR calculates the income necessary for a family to qualify for that mortgage amount (based on a 25% qualifying ratio for monthly housing expense to gross monthly income and a 20% down payment).

Shown below is a graph of the income needed to buy a median priced home in the country over the last few years. From 2012 to 2015, your income would have had to increase by over 38% to qualify for a home purchase at median prices. And the income requirement has accelerated even more dramatically this year as prices have steadily risen.

Bottom Line

Interest rates continue to remain low. However, some buyers may be waiting to save up a larger down payment. Others may be waiting for a promotion and more money. Understand that, while you are waiting, the requirements are also changing and spending time may cost you more money than you realize. And, as always, if I can answer any questions for you or provide you with more information, I am here to help!

If you are debating purchasing a home right now, you are most likely getting a lot of advice. Though your friends and family will have your best interests at heart, they may not be fully aware of your needs and what is currently happening in real estate. Buying or selling a home is one of the biggest emotional as well as financial decisions most people make in their lifetime, and taking the time to think it through carefully before you act is always wise.

Let’s look at whether or not now is actually a good time for you to buy a home. Where should you begin? Begin by asking yourself the following 3 questions:

1. Why am I buying a home in the first place?

This truly is the most important question to answer. Forget the finances for a minute. Why did you even begin to consider purchasing a home? For most, the reason has nothing to do with finances.

A study by the Joint Center for Housing Studies at Harvard University reveals that the four major reasons people buy a home have nothing to do with money:

A good place to raise children and for them to get a good education

A place where you and your family feel safe

More space for you and your family

Control of that space

What non-financial benefits will you and your family derive from owning a home? The answer to that question should be the biggest reason you decide to purchase or not.

2. Where are home values headed?

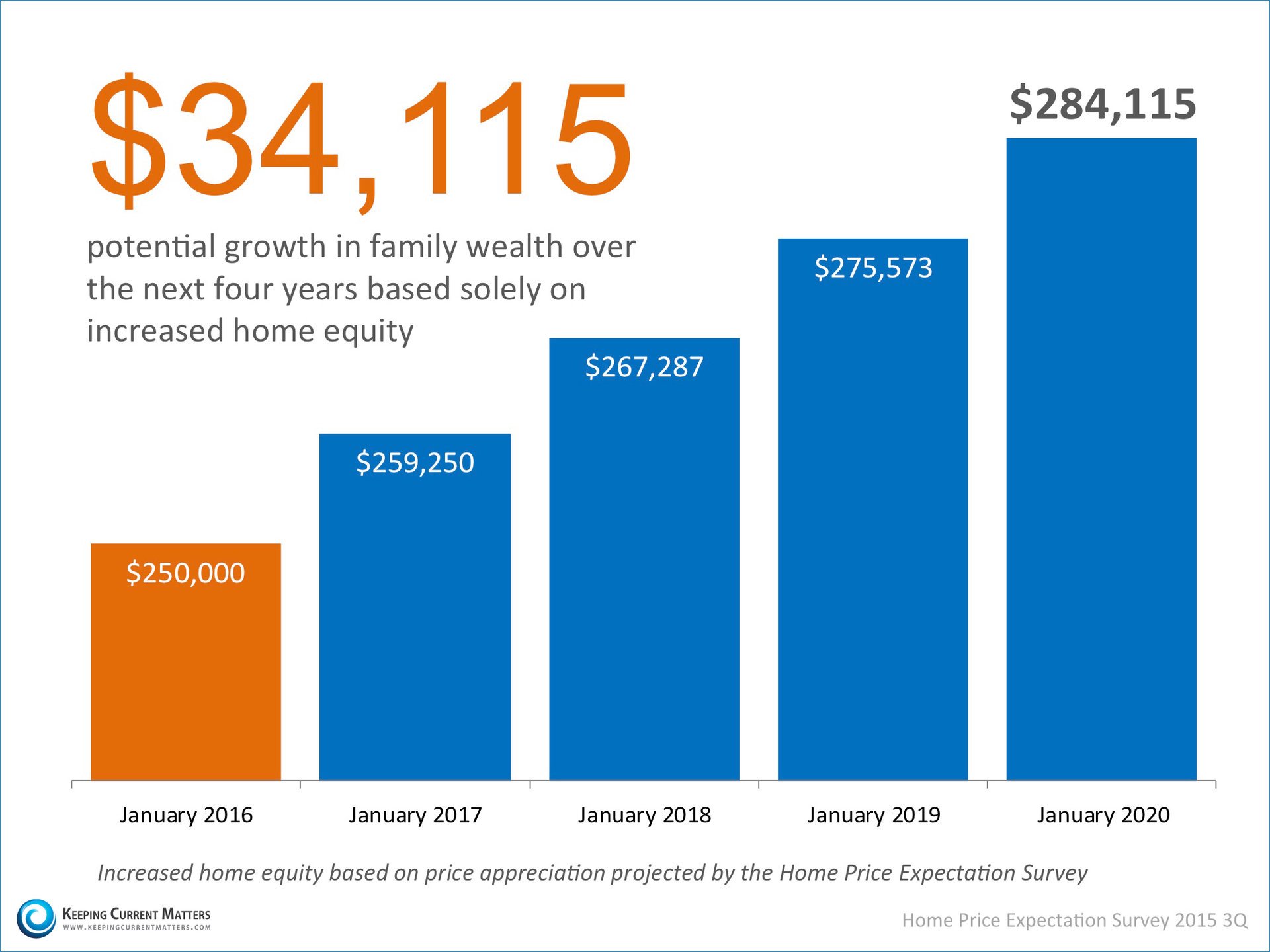

When looking at future housing values, Home Price Expectation Survey provides a fair assessment. Every quarter, Pulsenomics surveys a nationwide panel of over 100 economists, real estate experts and investment & market strategists about where prices are headed over the next five years. They then average the projections of all 100+ experts into a single number.

Here is what the experts projected in the latest survey:

Home values will appreciate by 4.1% in 2015.

The cumulative appreciation will be 18.1% by 2019.

Even the experts making up the most bearish quartile of the survey still are projecting a cumulative appreciation of over 10.5% by 2019.

So what does that really mean for you and your family?

The chart below was made using the Home Price Expectation Survey’s predictions:

If the experts are right and you were to purchase a home by January 2016 for $250,000, that home would appreciate by over $34,000 over the next four years! As we have reported before, homeownership is one of the best ways to build your family’s wealth. It creates a habit of thinking about and preparing for the future in ways that many other activities do not.

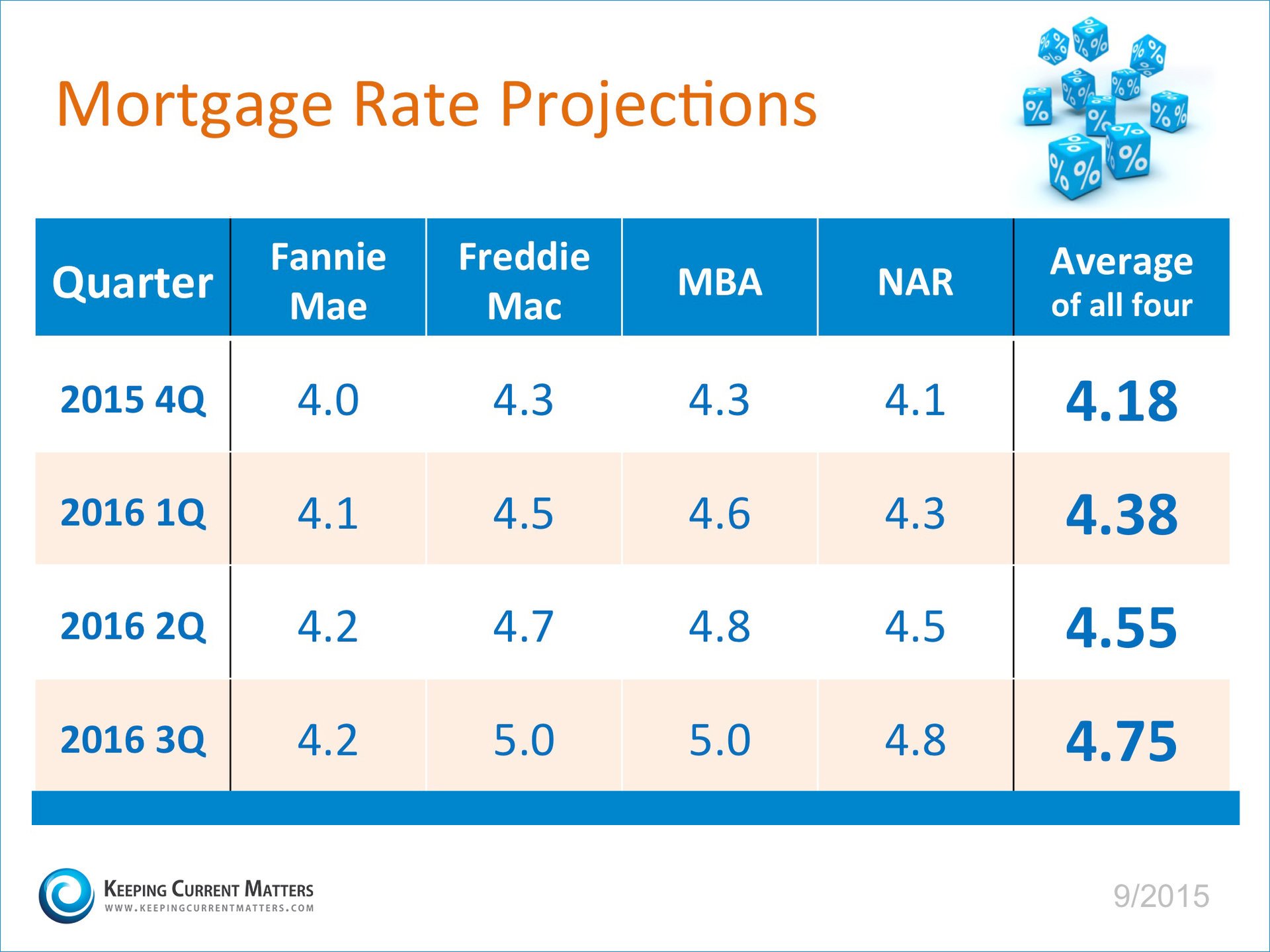

3. Where are mortgage interest rates headed?

A buyer must be concerned about more than just prices. The long term cost of a home can be dramatically impacted by an increase in mortgage rates. Although we have seen historically low interest rates for a longer period of time than many anticipated, the current rates are not likely to be available forever.

The Mortgage Bankers Association (MBA), the National Association of Realtors andFreddie Mac have all projected that mortgage interest rates will increase by approximately one full percentage point over the next twelve months as you can see in the chart below:

Bottom Line

Only you and your family will know for certain whether now is the right time to purchase a home. Answering these 3 questions will help you make that decision. And, as always, if I can be of service in some way or help you with other questions, please don't hesitate to let me know!

Have you noticed a recurring theme in the news as well as in my posts? More and more focus is being placed on homeownership as a means to creating wealth. The housing market has made a strong recovery, not only in sales and prices but also in the confidence of consumers and experts as an investment. In a New York Times editorial entitled, "Homeownership and Wealth Creation"it was explained:

“Homeownership long has been central to Americans’ ability to amass wealth; even with the substantial decline in wealth after the housing bust, the net worth of homeowners over time has significantly outpaced that of renters, who tend as a group to accumulate little if any wealth.”

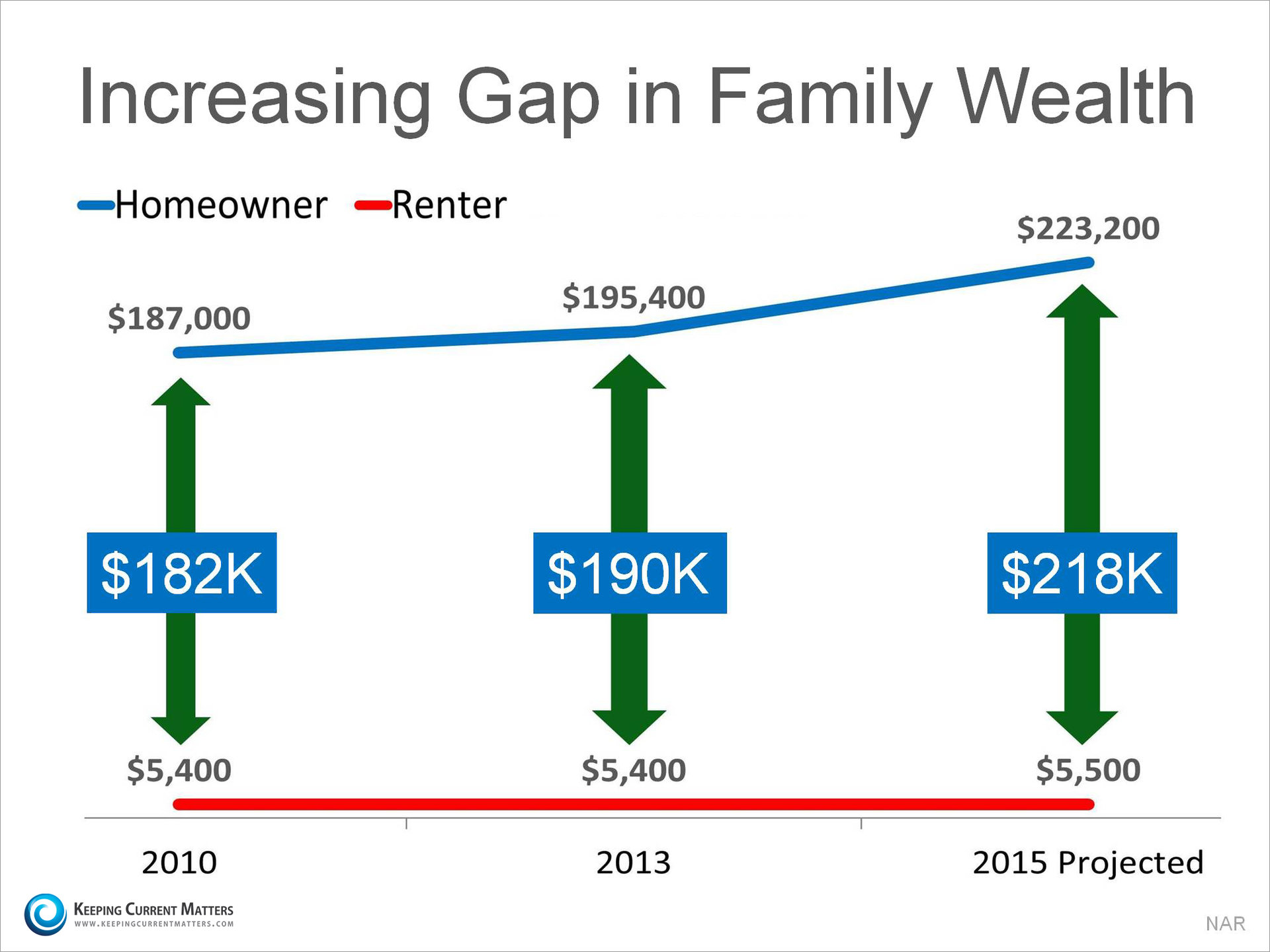

Many of the points that were made in the article are on track with the research that the Federal Reserve has also conducted in their Survey of Consumer Finances. The differences between homeowners and renters is startling:

The study found that the average net worth of a homeowner ($194,500) is 36x greater than that of a renter ($5,400).

The National Association of Realtors (NAR) expanded on the Federal Reserve’s research and projected that by the end of 2015, the average homeowner will have nearly 41x the net worth of a renter. Their findings are detailed in the graph below, and understanding the differences can make all the difference in your life!

One reason for this large discrepancy in net worth is the concept of ‘forced savings’ created by having a mortgage payment and was explained by the Times:

“Homeownership requires potential buyers to save for a down payment, and forces them to continue to save by paying down a portion of the mortgage principal each month.”

“Even in instances where renters have excess cash, saving a substantial amount is difficult without a near-term goal, like a down payment. It is also difficult to systematically invest each month in stocks, bonds or other assets without being compelled to do so.”

Bottom Line

“As a means to building wealth, there is no practical substitute for homeownership.” Homeownership creates a habit of savings and investment. If you are a renter who is considering making a purchase, sit with a local real estate professional who can explain the benefits of signing a contract to purchase over renewing your lease. And, as always, if I can answer any questions for you or be of assistance in some way, please don't hesitate to let me know!

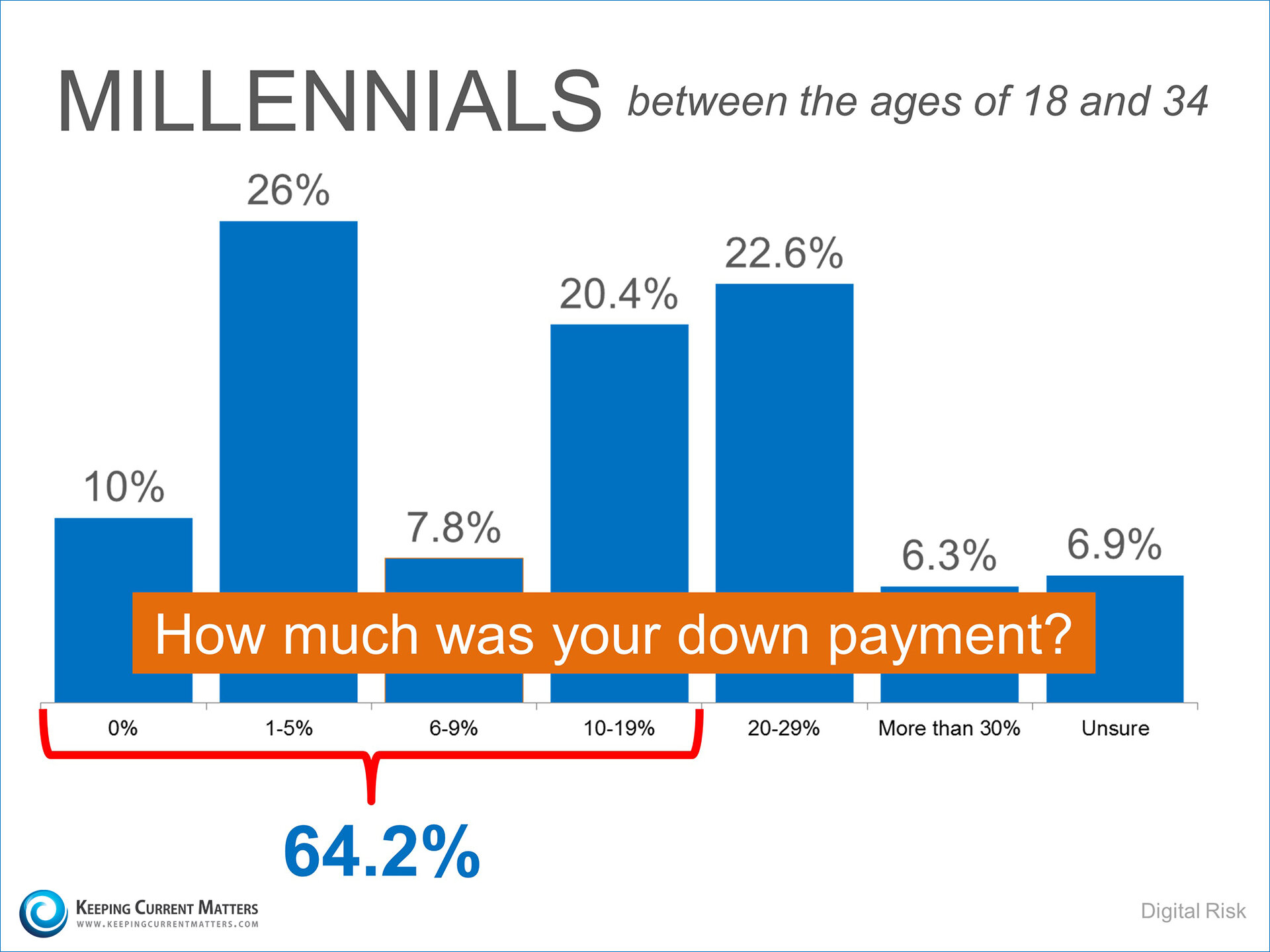

Digital Risk recently polled Millennials about the housing market. Among their findings was the fact that nearly two-thirds of that generation who have recently purchased a home have done so with less than 20% down, with 36% putting down less than 5%.

Here is a graph detailing the results:

This means that more and more Americans between the ages of 18 and 34 have stopped paying their landlord’s mortgage and have started building their own family’s wealth. Homeownership is definitely one way for families to build for the future!

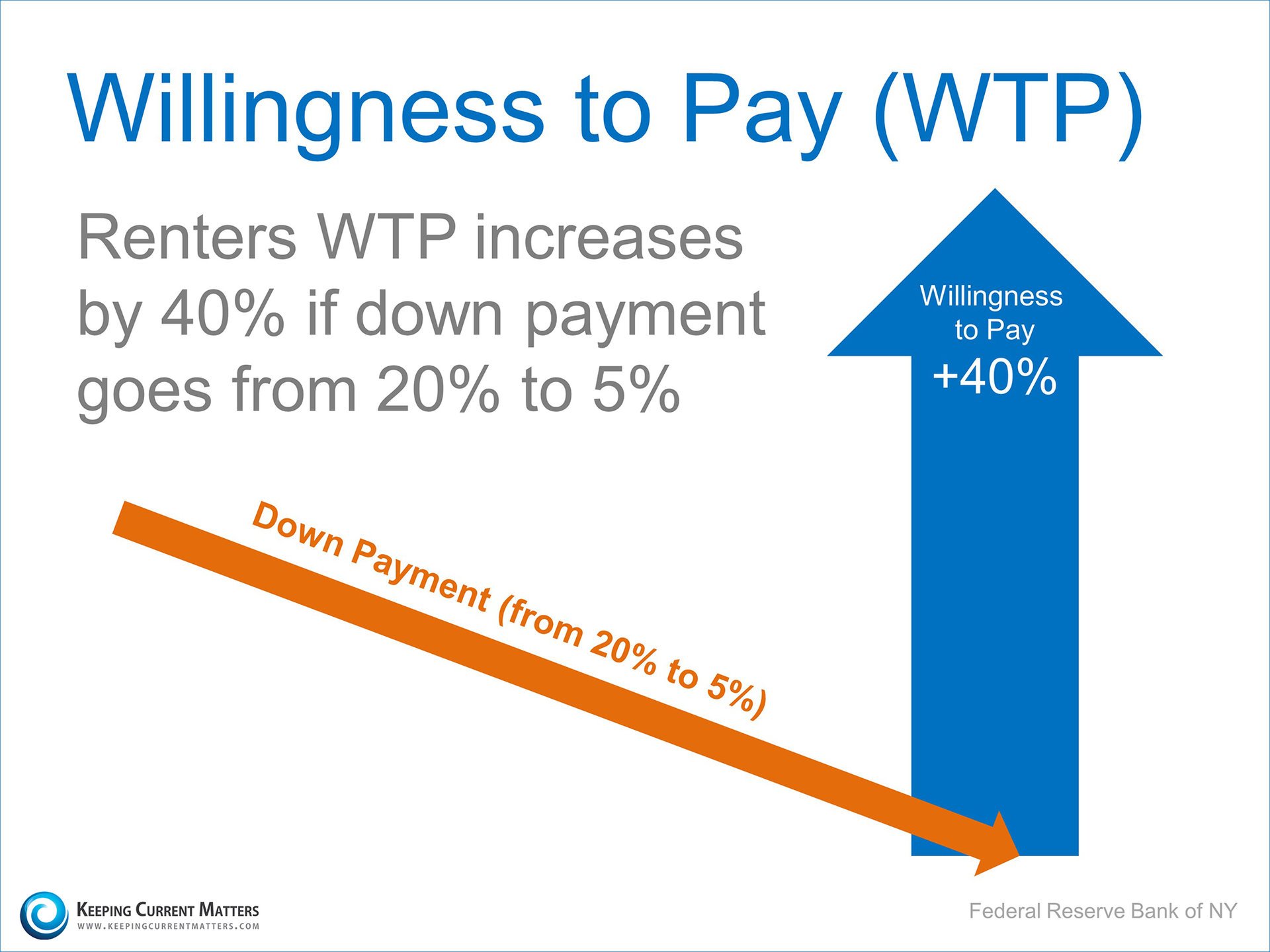

Millennials aren’t the only ones taking advantage of lower down payments.

The Federal Reserve Bank of New York found that if the down payment required to purchase a home went from 20% to 5%, a renter’s Willingness To Pay (WTP) increased by 40%. That's a significant shift in thinking, and one that can have a major impact on the housing market.

One problem is that thirty-six percent of Americans still believe a 20% down payment is always required when buying a home. Many renters may actually be able to enter the housing market sooner than they ever imagined with new programs available that allow less cash out of pocket. FHA, USDA, and VA loans may be options for those wanting to take the step up to home ownership but who may be unable to come up with the 20% down called for by a conventional mortgage. A reputable mortgage professional should be able to help you gather more information on options suitable to your situation.

Bottom Line

If you are one of the many renters now realizing that the home of your dreams is obtainable, contact a local real estate professional who can help you get started. Working with a great team of professionals can help make those dreams come true. And, as always, if I can anwer questions or be of help, please don't hesitate to let me know!

The big housing news last week was that the homeownership rate has dropped to 63.4% which represents the lowest rate in 48 years. That news definitely is making headlines and raising questions. To fully understand what this means, let's look at the story that created the headlines.

There is no doubt the homeownership rate has declined since the housing crisis. Given that many who bought into homes during that time were not well qualified and have dropped out of the ownership market, and given the overall impact of the housing crisis on the economy, it is not surprising that homeownership numbers decreased dramatically. Below is a graph showing the homeownership rate over the last twenty years. It skyrocketed during the housing boom but has steadily fallen since the bust:

The story behind the headline…

The dramatic fall in the rate over the past year must be looked at very closely. The rate is determined by the “number of households” who rent versus those who are owner occupied. Let’s assume you have nine friends that live on their own (thus forming a household); six of them own and three of them rent. That would mean that 66.6% (6 out of 9) of your friends that live on their own are homeowners.

Now, let’s assume you have another friend who has been living with his parents. He would not be considered a separate household because he lives within his parents’ household. Once that friend moves out of his parents’ home and gets a place of his own, he will become part of the household count. Let’s assume, since he is just starting out, that he moves into a rental. When he does, you now have ten friends that live on their own. If six still own their home and four of your friends now rent, the homeownership rate of your friends drops to 60% (6 out of 10). The number who own didn’t decrease; but the percentage decreased.

With the economy improving and job numbers looking better, more and more young adults are beginning to move out and get a place of their own. However, most will start living their independence in a rental situation thus driving the “percentage” of homeownership down. Auction.com explained the most recent drop in homeownership rate this way:

“This occurred as household formations popped, implying millennials are riding an improved labor market out of mom and dad’s house. Roughly a third of millennials live at home according to Census data, an elevated figure. Continued gains in the labor market will coax increased numbers out into their own places, a majority of which will be apartments, as this age cohort lacks the financial wherewithal to buy.”

What does this mean to the future of homeownership?

The great news is that study after study has shown that Millennials aspire to homeownership as they still see it as a major part of the American Dream. As they get more comfortable with their financial situation, many of the Millennials who finally made it out of their parents’ homes this year will become homeowners over the next several years. An increase in homeownership rates should follow. Does that mean we will achieve the record numbers achieved during the bubble? If we do, let's hope it's due to increasing prosperity across boundaries as more and more people are able to live the dream! And, as always, if you'd like more information or have questions, please ask. I'm here to help!

There has been a lot of discussion in the media about homeownership and whether it is a true vehicle for building wealth. A new report looks at the impact owning a home has on the financial wellbeing of people closing in on their retirement years (ages 55-64).

In recently released study by the Hamilton Project, "Ten Economic Facts About Financial Well-Being in Retirement," it was revealed that:

"Most households in the United States find retirement planning a daunting challenge, with good reason. Rising life expectancy and potentially exorbitant long-term care costs have increased the financial resources required to support oneself and one’s spouse in retirement and old age. For many segments of the population, negligible real wage growth has made the challenge all the more difficult. Furthermore, there are multiple dimensions of uncertainty when it comes to planning for those years, including returns on investments, health, longevity, Social Security benefits, and the level and type of support available from family members. Even with substantial planning, unanticipated events such as losing a job near retirement age, developing a serious illness, or the early death of a spouse can put pressure on even the most wellplanned retirement portfolios."

They study goes on to make the following salient points:

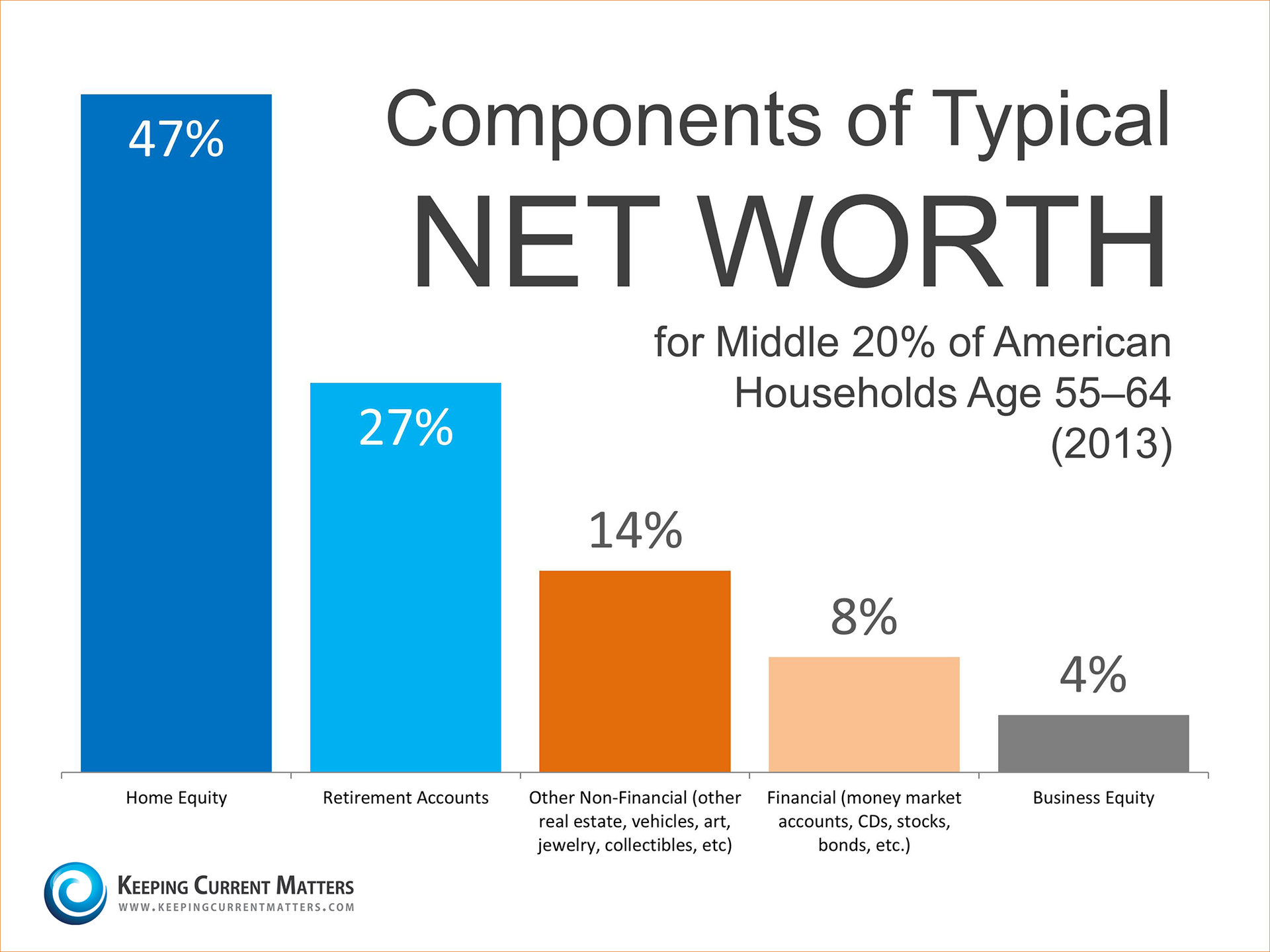

1. Middle-class households near retirement age have about as much wealth in their homes as they do in their retirement accounts.

“Over the past quarter century the largest single source of wealth for all but the richest households nearing retirement age has been their homes, which accounted for about two-fifths of net worth in the early 1990s and accounts for about one-third today.”

2. Home equity is a very important source of net worth to all but the wealthiest households near retirement age.

“Home equity is an important source of wealth for middle income households, accounting for more than one-third of total net worth for the second, third, and fourth quintiles of the net worth distribution… The fifth quintile has a much larger share in business equity—almost a quarter—than any other quintile. (The figure leaves out the bottom quintile of households because they have negative net worth. It is likely that these households will rely almost exclusively on Social Security in retirement.)”

Here is an asset breakdown for the middle 20% of Americans determined by median net worth ($165,720). Note the overwhelming percentage vested in home equity for this group:

The data from this study shows, once again, that what has been historicallly true remains true for many today. Homeownership plays a big role in building wealth for American families. Interested knowing more, or have questions? As always, please feel free to ask. I'm here to help!

The recent talk of Greece and its financial challenges has some questioning whether the U.S. could also return to the crisis we experienced in 2008. Some are looking at the rise in real estate values and wondering whether we are in the middle of another housing price bubble. This is a valid question, and one deserving of real consideration.

What actually is a price bubble?

Jack M. Guttentag, Professor of Finance Emeritus at the Wharton School of the University of Pennsylvania, in a recent article explained:

The question is being asked with increasing frequency, and also with great anxiety. The last housing bubble led to a financial crisis followed by a recession.

Many of those commenting on the question, however, don't understand what a price bubble is. It is NOT a marked rise in prices. Sharp price increases are common, and pose no threat to the stability of the economy whereas price bubbles are rare and do pose a threat.

A price bubble is a rise in price based on the expectation that the price will rise. Sooner or later something happens to erode confidence in continued price increases, at which point the bubble bursts and prices drop. What makes it a price bubble is that the cause of the price increase is an expectation that the price will increase, which sooner or later must reverse itself.”

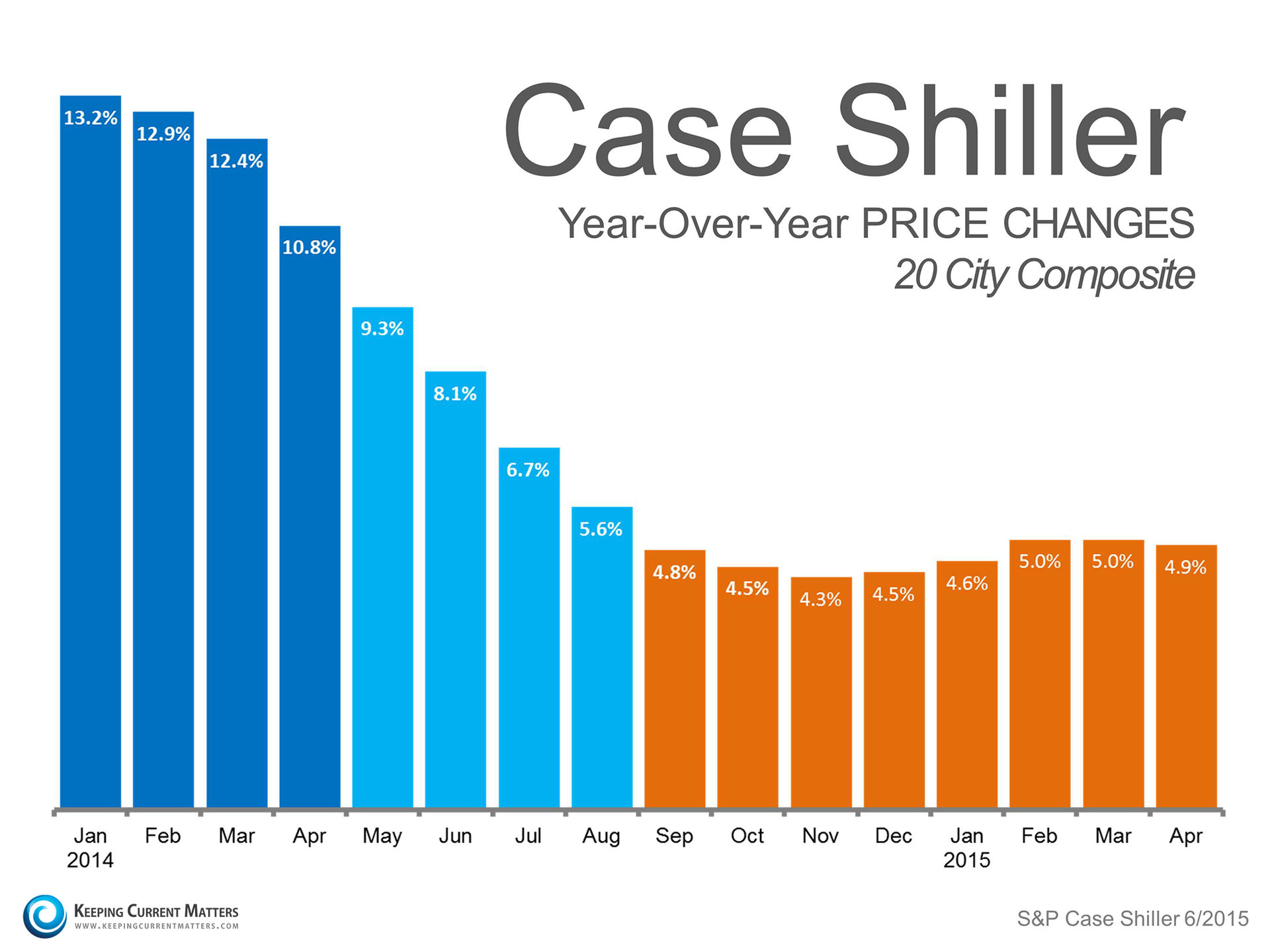

What are home prices doing?

Though home values are continuing to appreciate, the acceleration of the increases has slowed to relatively stable, year-over-year numbers which reflect a healthy housing market. Here is a chart showing year-over-year appreciation since January of last year:

We can see that appreciation rates have dropped from double digit numbers in January of 2014 to more normal rates of 5% or lower. These numbers are more consistent with historical price increases more closely tied to the rate of inflation.

Bottom Line

Are we looking at another housing price bubble this year? I think Nick Timiraos of the Wall Street Journal put it best in a recent tweet:

“Predictions of a new national home price bubble look unfounded for now, according to data.”

Would you like more information specific to your area? As always, please feel free to ask any questions you might have. I'm more than happy to help!

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link