Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

According to Freddie Mac, “Mortgage Rates Hit New 2016 High.”

“The 10-year Treasury yield dipped this week following the release of the Job Openings and Labor Turnover Survey. The 30-year mortgage rate rose another 5 basis points to 4.13 percent, starting the month 18 basis points higher than this time last year. As rates continue to climb and the year comes to a close, next week’s FOMC meeting will be the talk of the town with the markets 94 percent certain of a quarter-point-rate hike.

- 30-year fixed-rate mortgage (FRM) averaged 4.13 percent with an average 0.5 point for the week ending December 8, 2016, up from last week when it averaged 4.08 percent. A year ago at this time, the 30-year FRM averaged 3.95 percent.

- 15-year FRM this week averaged 3.36 percent with an average 0.5 point, up from last week when it averaged 3.34 percent. A year ago at this time, the 15-year FRM averaged 3.19 percent.

- 5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 3.17 percent this week with an average 0.5 point, up from last week when it averaged 3.15 percent. A year ago, the 5-year ARM averaged 3.03 percent.”

Why did rates go up?

Whenever there is a presidential election, there is uncertainty in the markets as to who will win. One way that this is noticeable is through the actions of investors. In an election year, as we get closer to the first Tuesday of November, many investors pull their funds from the more volatile and less predictive stock market and instead, choose to invest in Treasury Bonds.

When this happens, the interest rate on Treasury Bonds does not have to be as high to entice investors to buy them, so interest rates go down. Once the elections are over and a President has been elected, investors return to the stock market and other investments, leaving the Treasury to raise rates to make bonds more attractive again.

Simply put, the better the economy, the higher interest rates will go. For a more detailed explanation of the many factors that contribute to whether interest rates go up or down, you can follow this link to Investopedia.

The Good News

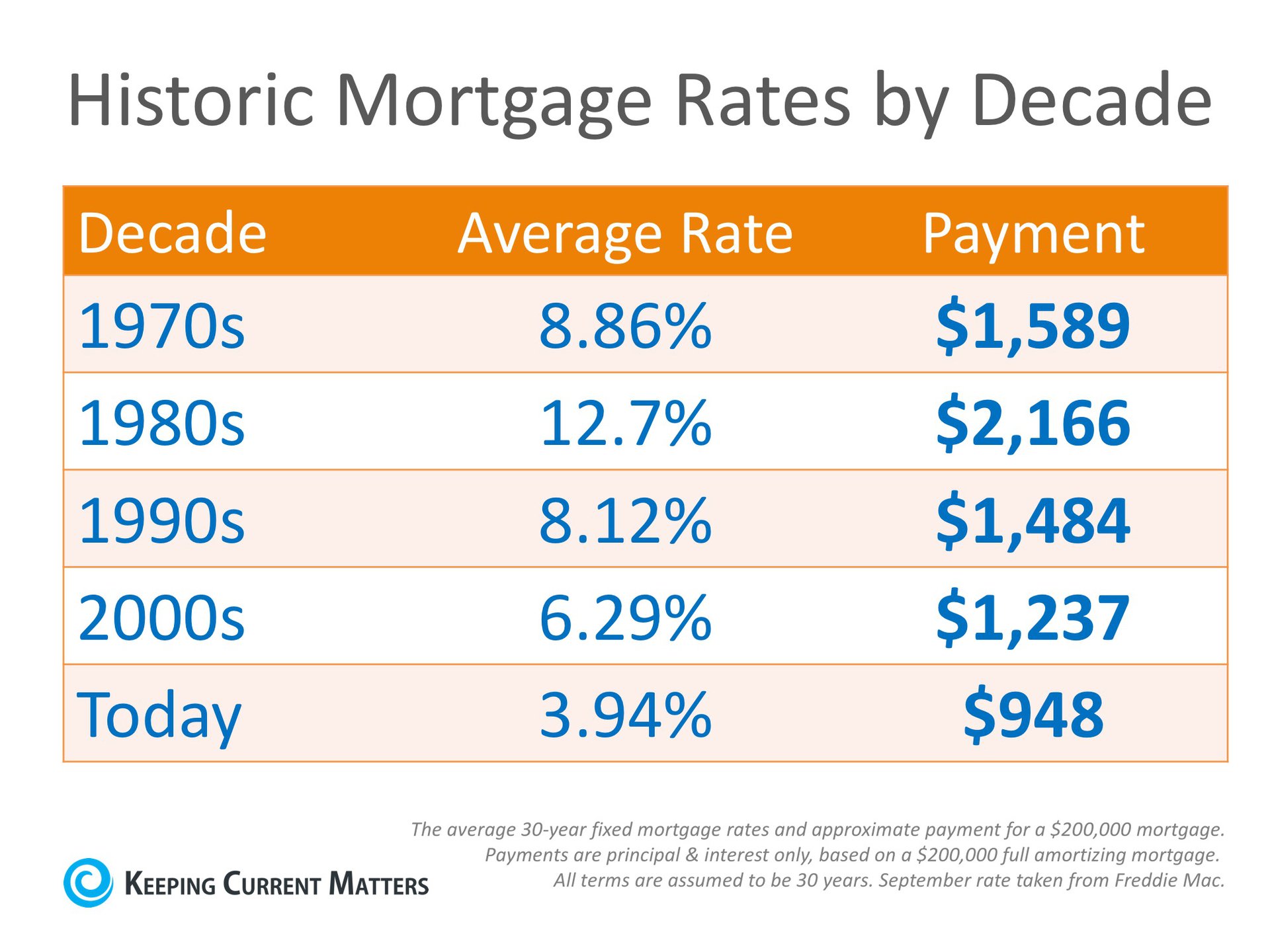

The good news is that even at slightly over 4%, rates are still significantly lower than they have been over the last 4 decades, as you can see in the chart below. And buying is still significantly less expensive than renting!

Any increase in interest rates will impact your monthly housing costs when you secure a mortgage to buy your home. A recent Wall Street Journal article points out that, “While still only roughly half the average over the past 45 years, according to Freddie Mac, the quick rise has lenders worried that home loans could become more expensive far sooner than anticipated.”

Tom Simons, a Senior Economist at Jefferies LLC, touched on another possible outcome for higher rates:

“First-time buyers look at the monthly total, at what they can afford, so if the mortgage is eaten up by a higher interest expense then there’s less left over for price, for the principal. Buyers will be shopping in a lower price bracket; thus demand could shift a bit.”

Bottom Line

Interest rates are impacted by many factors, and even though they have increased recently, rates would have to reach 9.1% for renting to be cheaper than buying. Rates haven’t been that high since January of 1995, according to Freddie Mac. As always, if you have questions, please feel free to ask. I’m here and happy to help!