Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Last week, an article in the Washington Post discussed a new ‘threat’ homebuyers will soon be facing: higher mortgage rates. The article revealed:

“The Mortgage Bankers Association expects that rates on 30-year loans could reach 4.8 percent by the end of next year, topping 5 percent in 2017. Rates haven’t been that high since the recession.”

How can this impact the housing market?

The article reported that recent analysis from Realtor.com found that –

“…as many as 7% of people who applied for a mortgage during the first half of the year would have had trouble qualifying if rates rose by half a percentage point.”

This doesn’t necessarily mean that those buyers negatively impacted by a rate increase would not purchase a home. However, it could mean that they would either need to come up with substantially more cash for a down payment or settle for a lesser priced home.

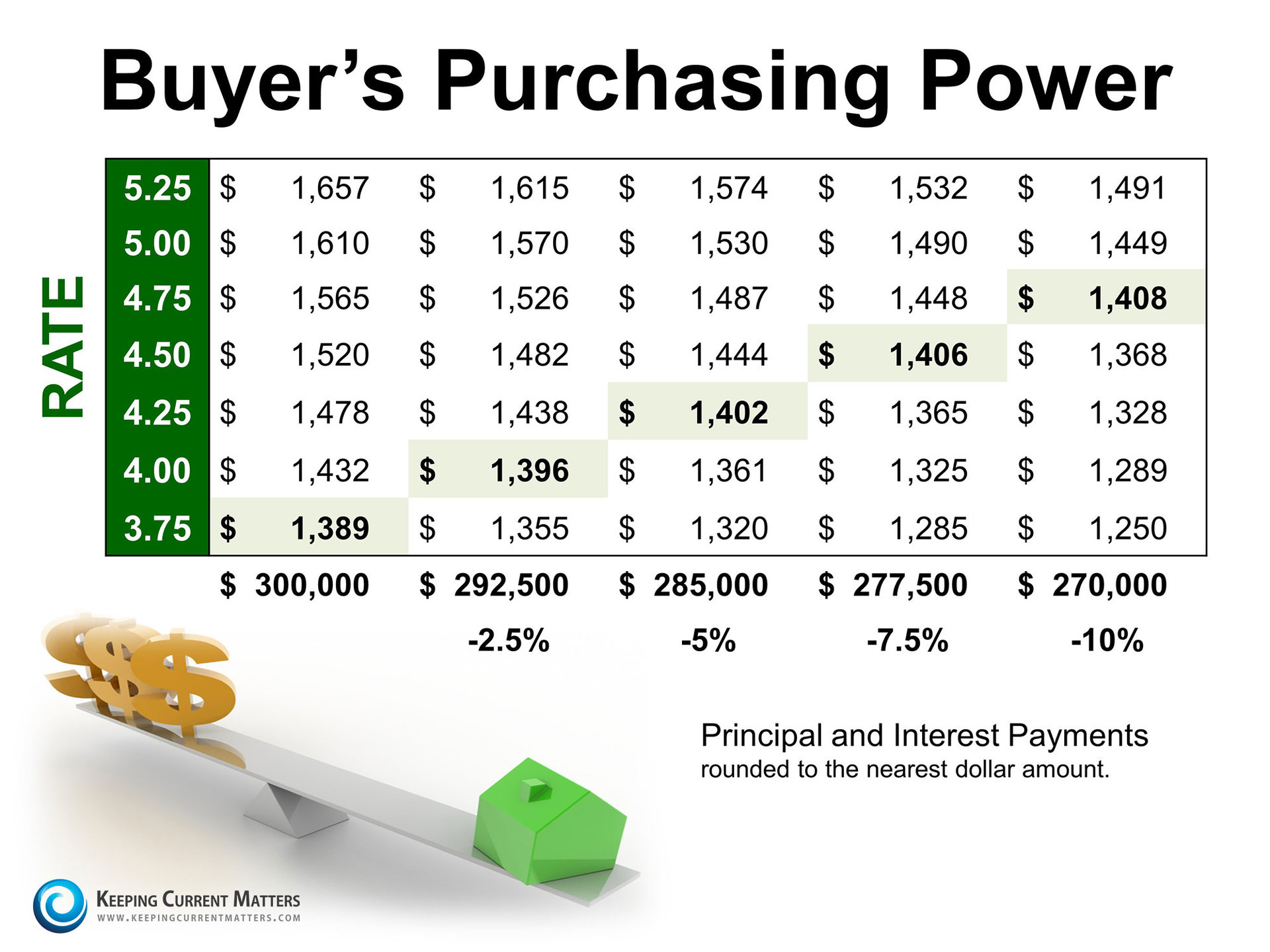

I find visual information helpful to me when making a decision. Below is a table showing how a jump in mortgage interest rates would impact the purchasing power of a prospective buyer on a $300,000 home. (Note that this chart does not include taxes and insurance in the payments provided.)

Bottom Line

Coupled with the rise in interest rates, the prices on homes throughout our area are continuing to rise. If you are considering a home purchase (either as a first-time buyer or as a move-up buyer), purchasing sooner rather than later may make more sense from a purely financial outlook. Are you wondering whether or not now is the time to buy? Sit down with a real estate professional to discuss your options before prices increase after the holiday season. And, as always, if I can answer any questions for you I am here to help!