Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Interest rates are still at record lows, but they are climbing and predicted to rise further by the end of 2017. Rising rates, increasing home values, and stricter lender requirements can make the home buying process challenging for many. An additional challenge for buyers is saving the funds necessary for a down payment. In a study conducted by Builder.com, researchers determined that nationwide, it would take “nearly eight years” for a first-time buyer to save enough for a down payment on their dream home.

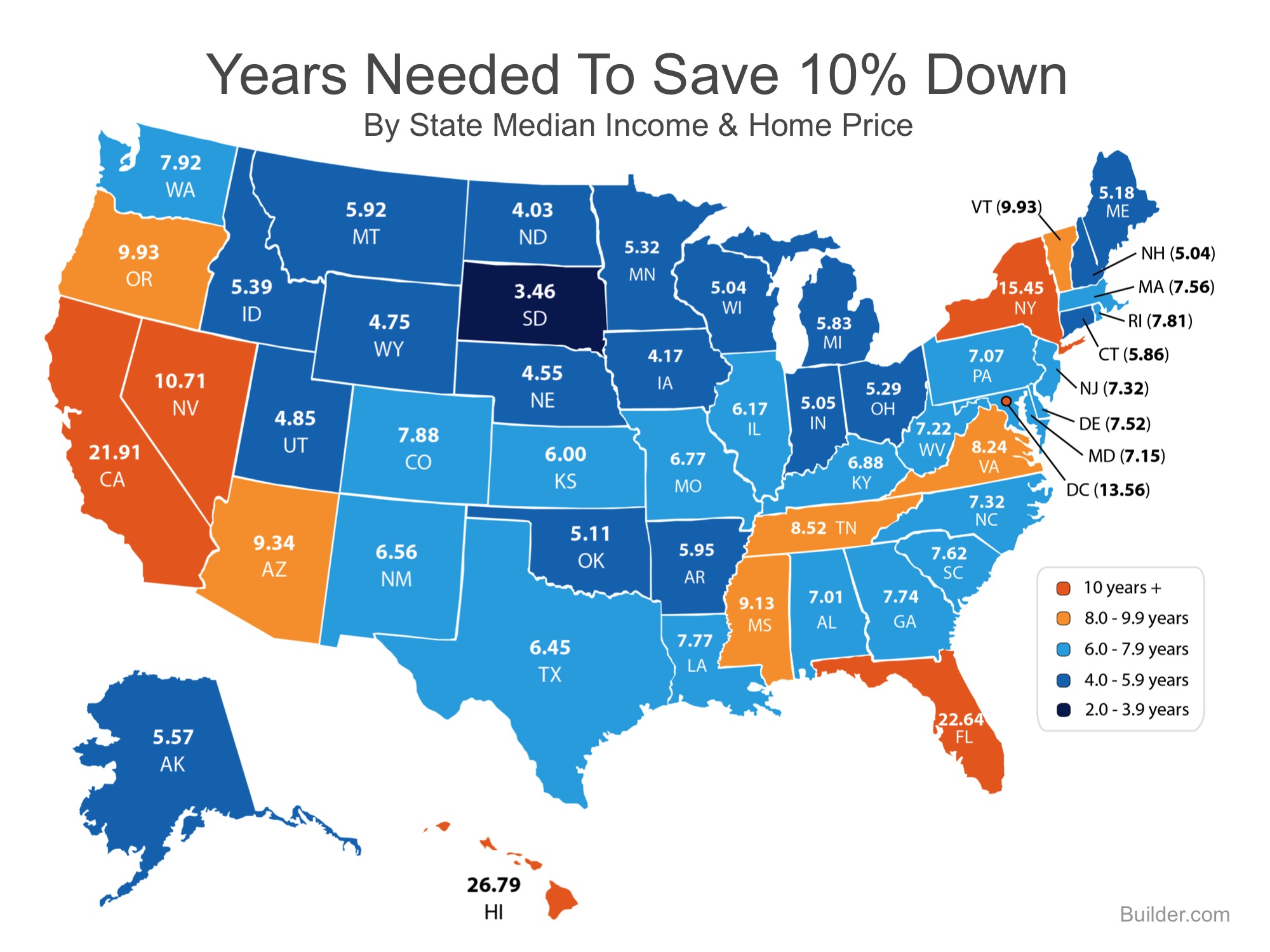

Depending on where you live, median rents, incomes, and home prices all vary. By determining the percentage of income a renter spends on housing in each state, and the amount needed for a 10% down payment, Builder.com was able to establish how long (in years) it would take for an average resident to save.

According to the study, residents in South Dakota are able to save for a down payment the quickest in just under 3.5 years. Below is a map created using the data for each state:

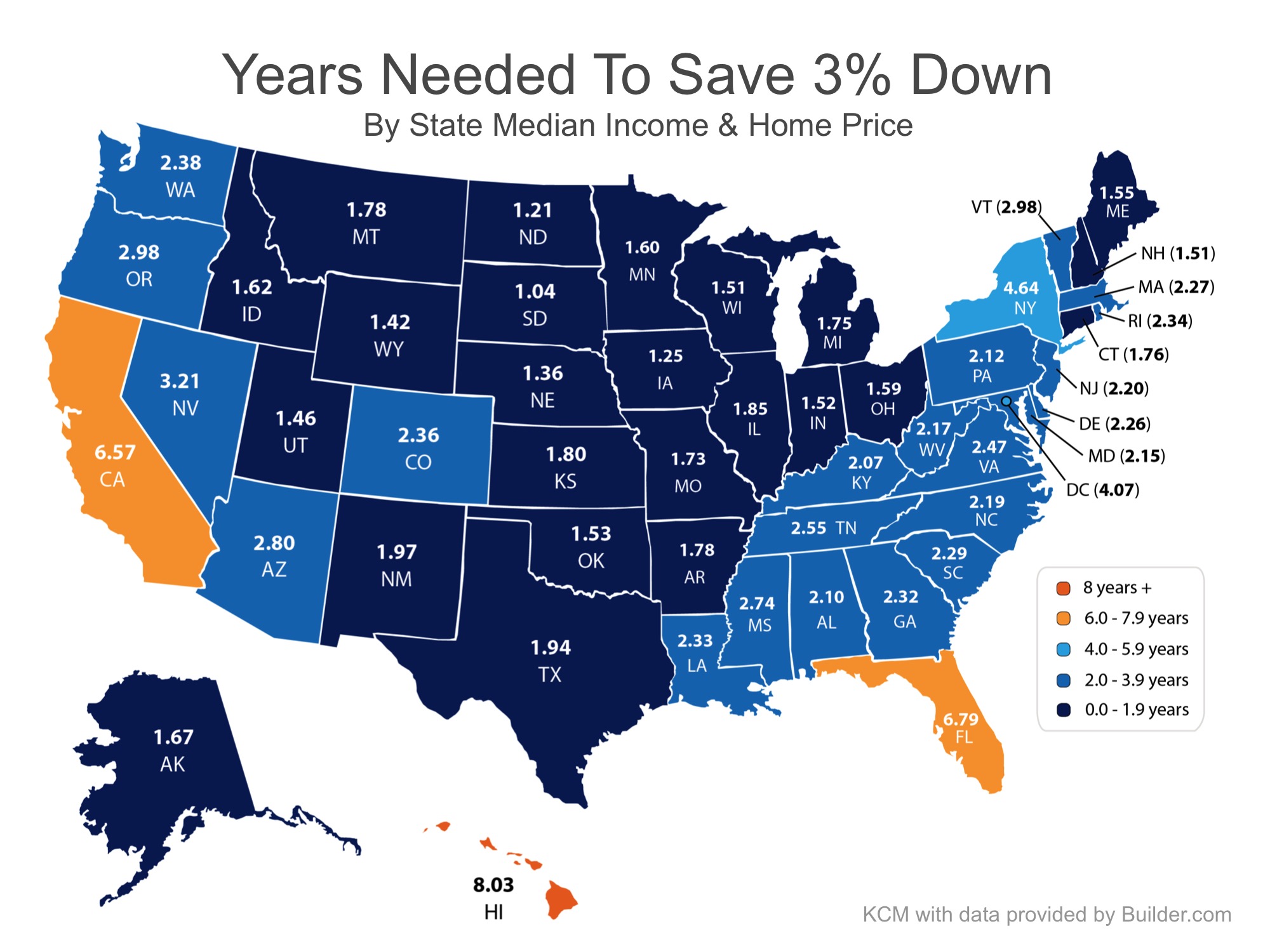

What if you only needed to save 3%?

What if you were able to take advantage of one of the Freddie Mac or Fannie Mae 3% down programs? Suddenly saving for a down payment no longer takes 5 or 10 years, but becomes attainable in under two years in many states as shown in the map below.

Bottom Line

A great lender can help you determine your purchasing power, what type of loan you are eligible for, and what kind of down payment you will need. And a professional financial advisor can help you create a plan to budget, save, and invest in your dream home. Whether you have just started to save for a down payment (or have been for years) you may be closer to your dream home than you think. And when you’re ready, I would be delighted to help you find that dream home and make it your own! As always, if you have questions or would like additional information, please don’t hesitate to ask. I’m here to help!